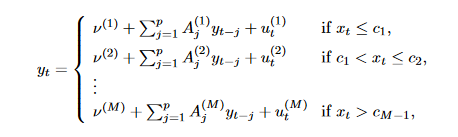

I have a var model :

y=dummy + other variables where dummy =1 if the firm is having a negative return on stock and 0 otherwise. Y is the return on stock. Is it appropriate to use the VAR model to study the impact of the dummy on y and other variables in this context?