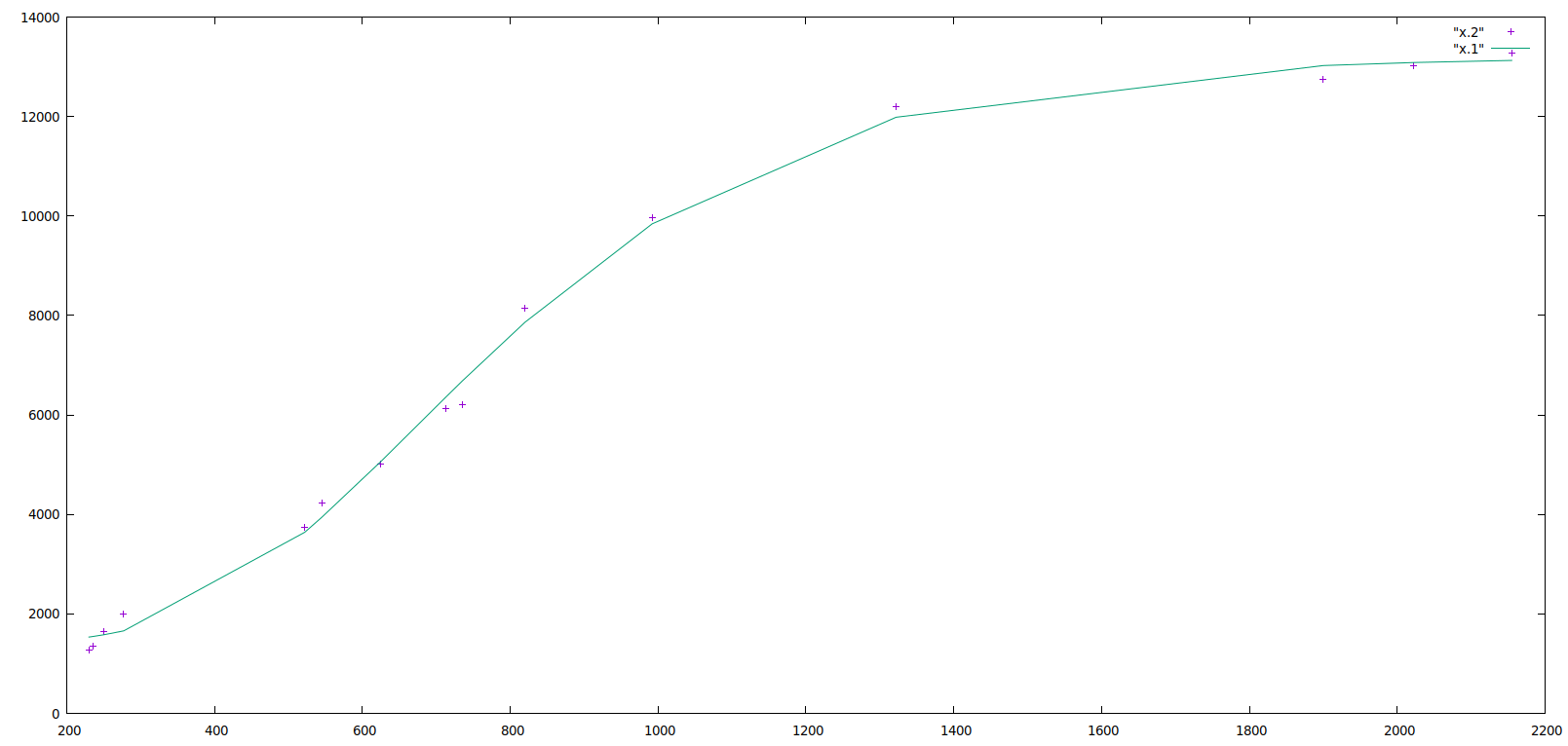

I have the following data:

y x

1275 230

1350 235

1650 250

2000 277

3750 522

4222 545

5018 625

6125 713

6200 735

8150 820

9975 992

12200 1322

12750 1900

13014 2022

13275 2155

I would like to find reasonable initial values for the model

$$y=\alpha+\beta_1\text{exp}(-\beta_2 e^{-\beta_3 x})+\epsilon$$

What I know:

For the Gompertz model, the inflection point satisfies

$$x=\frac{\text{log}(\beta_2)}{\beta_3}$$

For the Gompertz model we have

$$\lim_{x\rightarrow\infty} \beta_1\text{exp}(-\beta_2 e^{-\beta_3 x})=\beta_1$$

so presumably with an intercept we have

$$\lim_{x\rightarrow\infty} \alpha+\beta_1\text{exp}(-\beta_2 e^{-\beta_3 x})=\alpha+\beta_1$$

so we can set $\alpha+\beta_1=13275$, the maximum value of $y$ in the dataset.

However, I can't seem to combine what I know to find initial values.

I would like to find reasonable initial values and not rely on specifying an exhaustive grid of values.

Any ideas or suggestions would be appreciated.

Update:

I read on wikipedia that the halfway point is found to be

$${\displaystyle x_{\text{hwp}}=-{\frac {\ln\left(\frac{ln(2)}{\beta_2}\right)}{\beta_3}}}$$

I let $x_{\text{hwp}}=713$, the median of the $x$'s.

As previously stated, I have $$x=\frac{\text{log}(\beta_2)}{\beta_3}$$

I let $x=1000$, since a plot of the data shows that a possible inflection point is around there.

By software, this system of equation results in $\beta_2=0.279$ and $\beta_3=-0.0013$.

I (randomly) decided to let $\alpha=13275$ and $\beta_1=-13275$, where $13275$ is the maximum value of $y$.

The model then converges after 15 iterations to

$$\hat{y}=12934.4-14349.2\cdot\text{exp}(-0.1214e^{0.00257x})$$

which are reasonably close to my initial estimates. I'm not sure why it would make sense to have $\hat{\alpha}=13275$ and $\hat{\beta_1}=-13275$ though.