I have a dataset with around 15 independent variables. I am using a multi-regression model to fit the dataset. For model selection, I am using a backward elimination procedure based on the p-values. The adjusted R^2 for the model with all predictors is exactly 1. At this point, I concluded that maybe the model is also picking up noise. But, based on the model selection I removed 5 predictor variables and still the adjusted R^2 is 1. I am not sure if this correct or I am just modeling noise. Can someone comment on this?

$\begingroup$

$\endgroup$

1

-

5$\begingroup$ That shouldn't happen. You should be able to find out if all the residuals are 0. That is the only way the unadjusted R$^2$ can be 1. $\endgroup$– Michael R. ChernickCommented Jan 31, 2019 at 1:08

Add a comment

|

2 Answers

$\begingroup$

$\endgroup$

$\endgroup$

4

Dan and Michael point out the relevant issues. Just for completeness, the relationship between adjusted $R^2$ and $R^2$ is given by (see, e.g., here)

$$ R^2_{adjusted}=1-(1-R^2)\frac{n-1}{n-K}, $$ (with $K$ the number of regressors, including the constant). This shows that $R^2_{adjusted}=1$ if $R^2=1$, unless (see below) $K=n$.

$R^2=1$ occurs when all residuals $\hat u_i=y_i-\hat y_i$ are zero, as $$ R^2=1-\frac{\hat{u}'\hat{u}/n}{\tilde{y}'\tilde{y}/n}. $$ Here, $\hat u$ denotes the vector of residuals and $\tilde y$ the vector of demeaned observations on the dependent variable.

Dan discusses one reason to get an $R^2$ of 1. Another is to have as many regressors as observations, i.e., $K=n$.

Technically, this is because the $n\times K$ regressor matrix $X$ then is square. The OLS estimator $\hat\beta=(X'X)^{-1}X'y$ can then be written as (assuming no exact multicollinearity) $$ \hat\beta=(X'X)^{-1}X'y=X^{-1}{X'}^{-1}X'y=X^{-1}y $$ so that the fitted values $\hat y=X\hat\beta$ are just $\hat y=XX^{-1}y=y$, so that all residuals are zero.

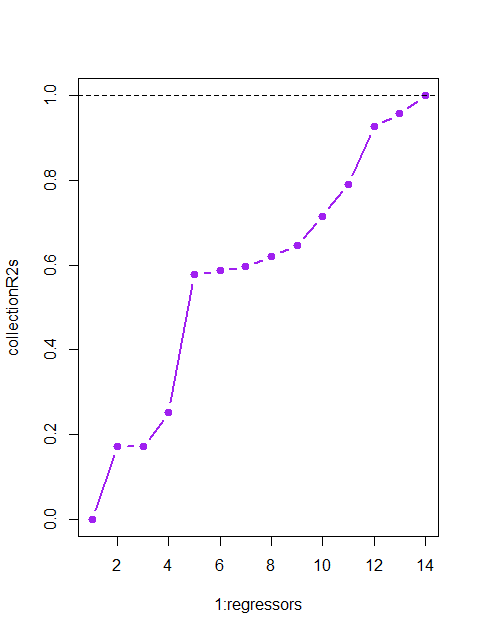

Here is an illustration using artificial data (code below), in which regressors are generated totally independently of $y$, and yet we achieve an $R^2$ of 1 once we have as many of them as we have observations.

Code:

n <- 15

regressors <- n-1 # enough, as we'll also fit a constant

y <- rnorm(n)

X <- matrix(rnorm(regressors*n),ncol=regressors)

collectionR2s <- rep(NA,regressors)

for (i in 1:regressors){

collectionR2s[i] <- summary(lm(y~X[,1:i]))$r.squared

}

plot(1:regressors,collectionR2s,col="purple",pch=19,type="b",lwd=2)

abline(h=1, lty=2)

When $K=n$, R however, correctly, does not report an adjusted $R^2$:

> summary(lm(y~X))

Call:

lm(formula = y ~ X)

Residuals:

ALL 15 residuals are 0: no residual degrees of freedom!

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 2.36296 NA NA NA

X1 -1.09003 NA NA NA

X2 0.39177 NA NA NA

X3 0.19273 NA NA NA

X4 0.51528 NA NA NA

X5 -0.04530 NA NA NA

X6 -1.28539 NA NA NA

X7 -0.72770 NA NA NA

X8 -0.14604 NA NA NA

X9 0.34385 NA NA NA

X10 -0.93811 NA NA NA

X11 2.23064 NA NA NA

X12 0.06744 NA NA NA

X13 0.21220 NA NA NA

X14 -2.29134 NA NA NA

Residual standard error: NaN on 0 degrees of freedom

Multiple R-squared: 1, Adjusted R-squared: NaN

F-statistic: NaN on 14 and 0 DF, p-value: NA

answered Jan 31, 2019 at 11:46

-

$\begingroup$ Do you want to expand on what u hat and y tilde are? I wonder how many cases the OP has as too few cases can easily lead to perfect prediction. $\endgroup$– mdeweyCommented Jan 31, 2019 at 15:37

-

$\begingroup$ Right, I should have spelled out all my notation in the first place. I agree it would be helpful information to know the sample size OP has access to. $\endgroup$ Commented Jan 31, 2019 at 15:42

-

$\begingroup$ By quoting an unnecessarily limited formula for the adjusted $R^2$ (which applies only to the ordinary regression situation but not to multiple regression) you arrive at an incorrect conclusion: the adjusted $R^2$ isn't even defined when there are as many regressors as observations. It's certainly not equal to unity in that case! $\endgroup$– whuber ♦Commented Feb 1, 2019 at 17:54

-

1$\begingroup$ Ouch, I should have seen that this was not the right expression to connect the adjusted and standard $R^2$. I hope that my edit fixes this. $\endgroup$ Commented Feb 1, 2019 at 19:39

$\begingroup$

$\endgroup$

An adjusted R squared equal to one implies perfect prediction and is an indication of a problem in your model. Adjusted R squared is a penalised version of R square, which is a way of describing the ratio of the residual sum of squares to the total sum of squares - as you approach 1 the implication is that there is no variation/deviation away from your model.

I would suggest you begin by looking at a correlation matrix, or put each predictor into your model individually to see which predictor is causing the issue.

In R, you will get a warning from lm: "essentially perfect fit..."

In the (single predictor) example below you will see that adjusted R square is less than 1 even when the correlation between y and x is greater than 0.99.

# create a data frame with some strongly correlated variables

myData<- data.frame(y = rnorm(n = 1000, mean = 0, sd = 1))

myData$x1<- myData$y

myData$x2<- jitter(myData$x1, factor = 10)

myData$x3<- jitter(myData$x1, factor = 1000)

# fit models

myModel1<- lm(y ~ x1, data = myData)

myModel2<- lm(y ~ x2, data = myData)

myModel3<- lm(y ~ x3, data = myData)

# output

summary(myModel1)

#> Warning in summary.lm(myModel1): essentially perfect fit: summary may be

#> unreliable

#>

#> Call:

#> lm(formula = y ~ x1, data = myData)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -4.551e-15 -1.200e-17 6.000e-18 2.090e-17 3.455e-16

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 1.404e-17 4.924e-18 2.852e+00 0.00444 **

#> x1 1.000e+00 5.085e-18 1.966e+17 < 2e-16 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Residual standard error: 1.553e-16 on 998 degrees of freedom

#> Multiple R-squared: 1, Adjusted R-squared: 1

#> F-statistic: 3.867e+34 on 1 and 998 DF, p-value: < 2.2e-16

summary(myModel2)

#>

#> Call:

#> lm(formula = y ~ x2, data = myData)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -1.996e-03 -9.643e-04 -1.996e-05 1.009e-03 2.034e-03

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 3.278e-06 3.647e-05 0.09 0.928

#> x2 1.000e+00 3.766e-05 26550.25 <2e-16 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Residual standard error: 0.00115 on 998 degrees of freedom

#> Multiple R-squared: 1, Adjusted R-squared: 1

#> F-statistic: 7.049e+08 on 1 and 998 DF, p-value: < 2.2e-16

summary(myModel3)

#>

#> Call:

#> lm(formula = y ~ x3, data = myData)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -0.214135 -0.097828 -0.003721 0.099000 0.226453

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) -0.001598 0.003602 -0.444 0.657

#> x3 0.983900 0.003685 266.982 <2e-16 ***

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Residual standard error: 0.1136 on 998 degrees of freedom

#> Multiple R-squared: 0.9862, Adjusted R-squared: 0.9862

#> F-statistic: 7.128e+04 on 1 and 998 DF, p-value: < 2.2e-16

cor(myData$x1, myData$x2)

#> [1] 0.9999993

cor(myData$x1, myData$x3)

#> [1] 0.9930721