It doesn't!

In general:

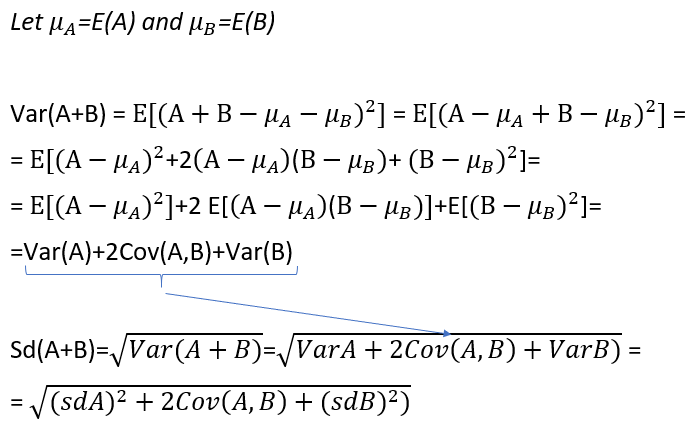

Var(A+B) = Var(A) + Var(B) + Cov(A, B)

The additive property only holds if the two random variables have no covariation. This is almost a circular statement, since a legitimate definition of the covariation could be:

Cov(A, B) = Var(A) + Var(B) - Var(A + B)

This means that the covariance measures the failure of the additive property of variance.

This leads to the true heart of the matter, the covariance is bi-linear:

Cov(A_1 + A_2, B) = Cov(A_1, B) + Cov(A_2, B)

Cov(A, B_1 + B_2) = Cov(A, B_1) + Cov(A, B_2)

For an intuitive understanding of this, I'll link to the wonderful: How would you explain covariance to someone who understands only the mean?. In particular, see @whuber's answer.