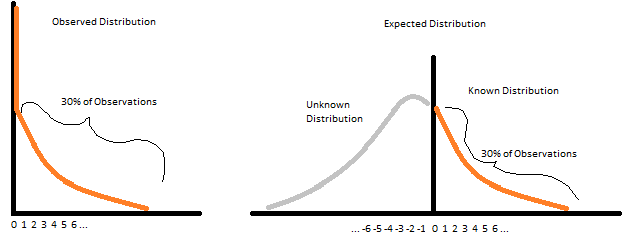

So, I've got a(n assumed) normal distribution that is left bound by 0, and I'm trying to extrapolate what would happen if the distribution could go negative.

Given a portion of the right tail of a normal distribution, is there a good method for building out the rest of the distribution?

For instance, in the below image, taking the observations at 0 and estimating the grey unknown distribution:

Edit:

To clarify, in most cases we'll know the second and third standard deviations (inferred from the percent of observations on the right side of the curve) from the mean, but not the mean itself - and, we want to find the mean an plot the unknown distribution (grey in the above picture).

Admittedly, I'm rusty in this area, so forgive me if this is a poor question.

Would it make sense to take the distance between the far right 2.1% of observations, call that the standard deviation and infer the mean and variance form that?