I am working with the Boston data set in R.

I have read that random forest should be able to deal with untransformed data. In my example I do a log transformation of the dependent variable. My variance explained goes from 54% to 94%.

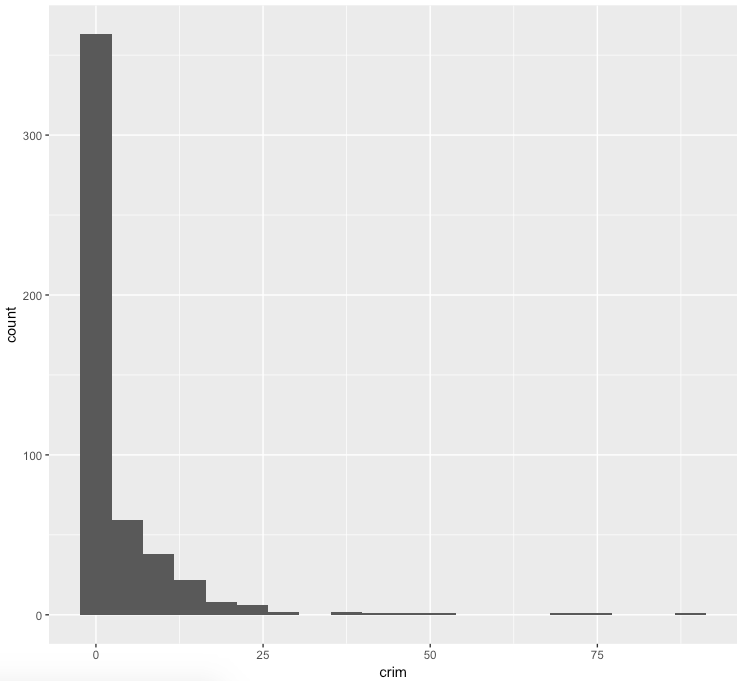

Here is what the original dependent variable looks like.

I run a random forest model without any transformation to the data set. Our dependent variable is crim.

library(randomForest)

randomForest(crim ~., Boston)

#variance explained is 54%

Once I do a log transformation of crim(to make the distro more normal) the variance explained jumps to 95%!!

randomForest(log(crim) ~., Boston)

#variance explained is 95%

Since this is a monotonic transfromation. I did not think it would have an impact on a tree based model. Can someone provide some intuition on why this might be the case? Thank you