I am running an impulse response function in R, using the package vars.

My data has 3 variables, the inflation (Brazilian CPI, or IPCA), the exchange rate and the output gap.

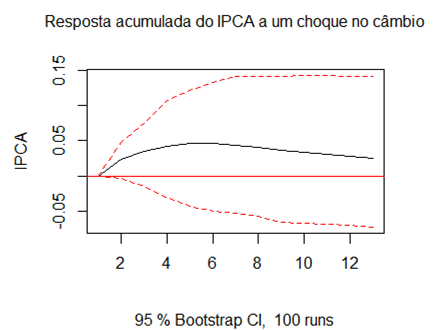

My goal is to calculate the exchange rate pass-through (both the maximum impact and the lag), and I am following and academic recommendation to add the output gap (as the monthly industrial production with HP filter).

The pass-through I am interested in is exchange rate -> CPI. The output gap is of my interest only in the way it impacts this pass-through relation. So I wrote the code as:

model_irf <- vars::irf(model_var,

impulse = "Exchange Rate",

response = "CPI",

n.ahead = 12,

cumulative = TRUE)

This gives me the expected response of variable “CPI” t+12 to a unit change in variable “Exchange Rate”.

I imagine (from macroeconomic theory) the output gap impacts the magnitude of the pass through, so in periods of larger output gap companies have less space to increase prices; relation that is not visible in this model I wrote.

My question is: How is the output gap related to the IRF I calculated? (Or if the model is wrong and I should write it differently to test this assumption)

Thank you very much for your time!