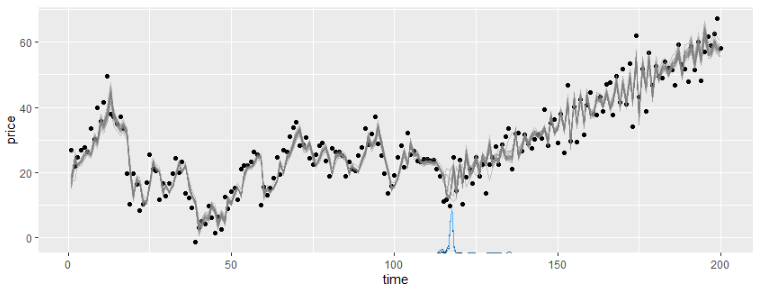

I have a time series with nonstationary data. Looking at the plot of the data it is clear that there are structural breaks. As data follow the stochastic process, I want to build Markov Switching Model, and due to nonstationary data, Markov trend is needed.

I want to implement the following model:

$$ y_t = (\alpha_0 t + \alpha_1 \sum_{i=1}^t s_i) + \beta_1 y_{t-1} + ... + \beta_k y_{t-k} + \sum_{i=1}^t \epsilon_t $$

which is introduced in this article.

However, this article is the only reference I have about Markov trend. Also, I don't really know how to start the implementation. Usually, I use MSwM R-package, but it doesn't contain Markov trend.

Does anybody have other references for Markov trend in Markov Switching Model? Even better would be any tips on how to implement the model. For me, the most problematic part is what to do with $s_i$ as it should be determined by the model - as far as I understand...