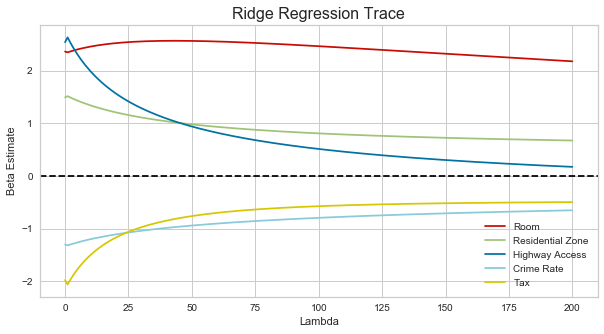

From my understanding, Ridge regression tends to shrink coefficients towards 0 as lambda increases. However, it seems this is not always the case - for features which are more statistically significant, Ridge Regression can increase their coefficient as lambda increases. Why is this? And how does the Ridge penalty cause this?