After having run the following regression in Stata

regress y x1 x2 ... xn [weight=w], robust

I given the following table:

Is there a way to get the confidence interval from the coefficient, robust standard errors, and number of observations?

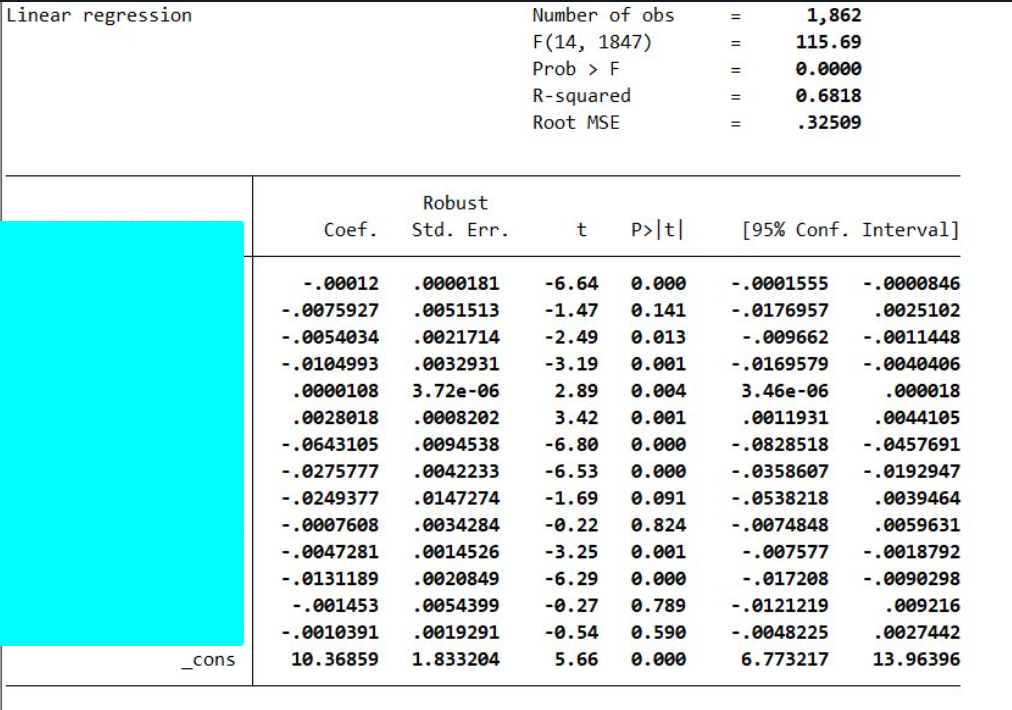

After having run the following regression in Stata

regress y x1 x2 ... xn [weight=w], robust

I given the following table:

Is there a way to get the confidence interval from the coefficient, robust standard errors, and number of observations?

No, you need the covariances as well.

Take a single covariate model $$ E[y \vert x] = \alpha + \beta x = m(x)$$

The 95%CI for $m(x)$ with a largish sample is $$m(x) \pm 1.96 \cdot SE(m(x))=m(x) \pm 1.96 \cdot \sqrt{SE(\alpha)^2+x^2 \cdot SE(\beta)^2+ 2 \cdot x \cdot Cov(\alpha,\beta)}$$

Stata stores the covariance on the off-diagonal elements of e(V) matrix. You can see it with

matrix list e(V)

With many covariates, the math gets messy quickly since there are many pairwise covariances. You can avoid doing this by hand by using margins or lincom.