Problem statement:

I am using a simple linear regression with outcome $y$ and single predictor $x$ of the form:

$$ y_i \sim N(\mu_i, \sigma) \\ \mu_i = \beta_0 + \beta_1x_i $$

I assume fitting $\beta_0, \beta_1$ with maximum likelihoood (although if other method works better for the purpose of this question, I can use that). Then, I observe a new set of outcomes $\bar{y}$ for a (known) new set of predictors $\bar{x}$ which I assume come from the same process. I then assume a regression is fitted independently to $\bar{x}, \bar{y}$ obtaining $\bar{\beta}_0, \bar{\beta}_1$.

Is there an analytical way to use the original fit to get something like a "prediction interval" for $\bar\beta_1$? I am looking for an interval with the expected coverage properties for $\bar\beta_1$ - the estimate of the slope from $\bar{x}, \bar{y}$. I assume this is going to be noticeably wider than the confidence interval as there's the additional uncertainty arising from sampling $\bar{y}$ and constructing the estimate based on those samples.

I could obviously use simulations to obtain that interval, but I am curious if there is a more elegant way.

Background:

I am attempting to do something akin to cross validation for testing the extent that each of a set of possible summaries is "reproducible" - having $N$ replicates, intuitively, a summary is good, if summarising $N - K$ replicates of the experiment lets me predict the summary the remaining $K$ replicates well. One of the summaries I am experimenting with is a slope from a regression model, so I'd like to develop the expected prediction interval if the model was actually capturing the data well.

Code example:

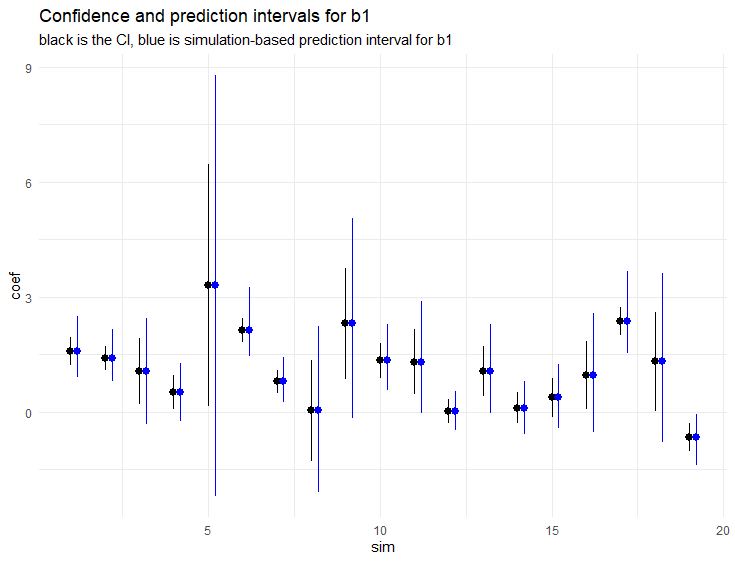

The following code shows the problem and solution with simulations in R.

In each simulation, I am trying to use the linear fit to $x,y$ to construct an interval that would contain $\bar{\beta}_1$ in 95% of cases. I use the confidence interval and then I use simulations to construct a "prediction" interval.

x <- rep(0:5, times = 4)

xbar <- rep(0:5, times = 2)

N_sims <- 100

#Pre-allocate

y <- matrix(NA_real_, nrow = N_sims, ncol = length(x))

ybar <- matrix(NA_real_, nrow = N_sims, ncol = length(xbar))

b1 <- numeric(N_sims)

b1ci <- matrix(NA_real_, nrow = N_sims, ncol = 2)

b1bar <- numeric(N_sims)

b1pred_sim <- matrix(NA_real_, nrow = N_sims, ncol = 2)

for(i in 1:N_sims) {

# Choose the true values randomly

# The results are quite similar whether I choose

# those separately for each simulation or

# once at the begining of the script

true_b0 <- 1 + rnorm(1)

true_b1 <- 0.5 + rnorm(1)

true_sigma <- 1 + rlnorm(1)

y_ <- rnorm(length(x), true_b0 + x * true_b1, sd = true_sigma)

y[i,] <- y_

fit <- lm(y_ ~ x)

b1[i] <- coef(fit)["x"]

b1ci[i,] <- confint(fit)["x",]

## Calculate the prediction interval with simulations

N_inner_sims <- 1000

sims_b1bar <- numeric(N_inner_sims)

for(j in 1:N_inner_sims) {

coef_sim_norm <- mvtnorm::rmvnorm(1, coef(fit), vcov(fit))

# Transform to T distribution

dof <- length(x) - 2

coef_sim <- coef_sim_norm / sqrt(rchisq(2, dof) / dof)

ysim <- rnorm(length(xbar), coef_sim[1] + xbar * coef_sim[2], sd = sigma(fit))

fitsim <- lm(ysim ~ xbar)

sims_b1bar[j] <- coef(fitsim)["xbar"]

}

b1pred_sim[i,] <- quantile(sims_b1bar, c(0.025,0.975))

## Actually fit the new data

ybar_ <- rnorm(length(xbar), true_b0 + xbar * true_b1, sd = true_sigma)

ybar[i,] <- ybar_

fitbar <- lm(ybar_ ~ xbar)

b1bar[i] <- coef(fitbar)["xbar"]

}

cat("Coverage CI: ", mean(b1bar >= b1ci[,1] & b1bar <= b1ci[,2]))

cat("Coverage prediction - sims: ",

mean(b1bar >= b1pred_sim[,1] & b1bar <= b1pred_sim[,2]))

Due to the simulations this is quite slow, but a typical result is something like:

Coverage CI: 0.81

Coverage prediction - sims: 0.96

so CI is too narrow while the simulations appear (at least approxiamtely) well calibrated. So the question is if I can get something like b1pred_sim analytically. Note that b1pred_sim is just appropriately widened CI: