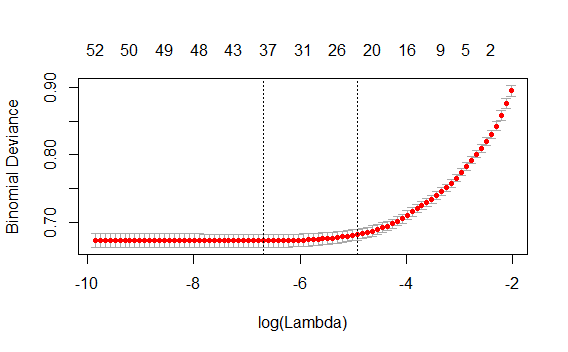

I'm not sure why you say that the deviance never decreases; it is certainly decreasing at large values of $\log(\lambda)$ on the rightmost edge of the plot to the left. However, the deviance is relatively flat over a large range of values of $\log(\lambda)$. Yet shrinkage is being applied, as the values on the upper x-axis (side = 3) indicate: the number of variables in the model declines consistently and markedly over the region of no or little change in deviance.

What this shows is that for models over this region, up to about $\log(\lambda) = -6$, shrinkage is being applied without affecting the CV fit of the model as assessed via CV binomial deviance. This is good, as it indicates that the elastic net is doing what you wanted it to, to perform feature selection whilst handling correlated covariates.