I have 295 observations of two variables, of which here are a few:

Date Close price

1/04/14 0:00 478.72

2/04/14 0:00 437.51

3/04/14 0:00 447.08

4/04/14 0:00 448.88

5/04/14 0:00 464.83

6/04/14 0:00 460.70

7/04/14 0:00 446.22

8/04/14 0:00 450.46

9/04/14 0:00 440.20

10/04/14 0:00 360.84

11/04/14 0:00 420.06

12/04/14 0:00 420.66

13/04/14 0:00 414.95

14/04/14 0:00 457.63

15/04/14 0:00 520.12

16/04/14 0:00 529.16

The first variable is the date plus time stamp "0:00" and the second variable is the price at that date. My whole data set spans 1/4/2014 till 20/1/2015 with daily observations.

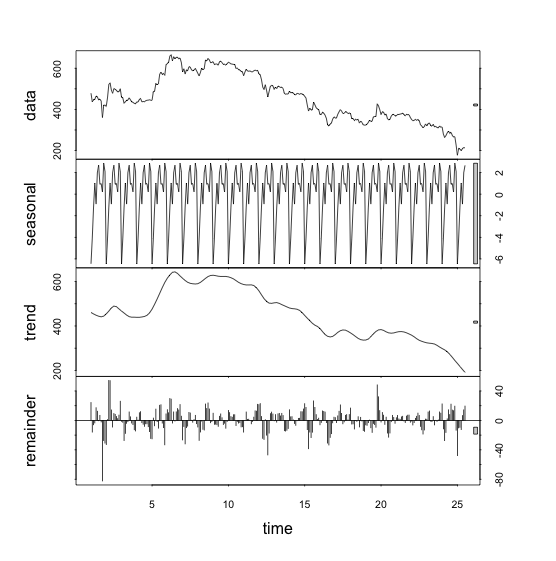

I want to decompose this data into two components, trend and errors. I know stl is mainly for seasonal data, but I use the following code, setting the value of s.window to be large to negate the seasonality component.

btc.ts<-ts(btc.csv$Close.Price,frequency=12)

decomp<-stl(btc.ts,s.window=10000)

plot(decomp)

There are a few issues here, the frequency of my data is daily, and frequency = 12 is not correct, but my hopes are that I just want to extract the trend component of the stl and use the zoo package:

trend<-decomp$time.series[,"trend"]

td<-seq(as.Date("2014/4/1"),as.Date("2015/1/15"),"days")

trendz<-zoo(x=trend,order.by=td)

The reason for this is that the trend component found in stl looks the best out of all my approaches, as shown below:

Now, what I want to do is fit a polynomial to model the trend, the issue I am having here is that I cannot use 'td' in the following command (natural splines):

trendz.fit<-lm(trendz~ns(td+I(td^2)+I(td^3)))

as td is a 'date' object. I just want to have something like : trend (t) = a + bt + c(t^2) + d(t^3)..

What can I do to achieve this? How does one usually treat regressions with one of the variables being time/date?

Any suggestions are appreciated, thanks