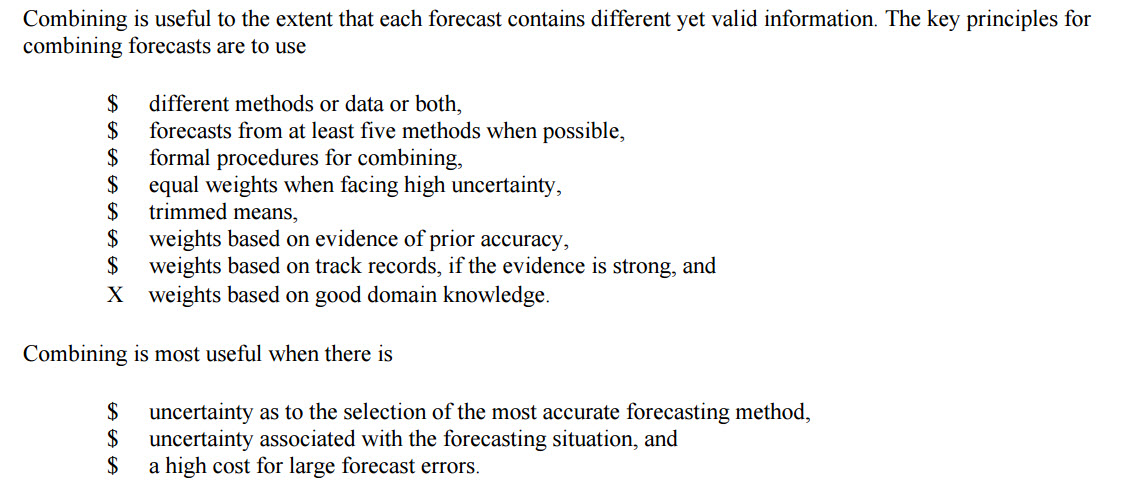

Combination Forecasting can be produced by simply averaging different forecasts or employing more complex techniques (see Makridakis, 1989; De Gooijer and Hyndman, 2006; Goodwin, 2009; Pesaran and Pick, 2011). The major principle of forecast averaging is simply by computing the average of two forecasts for the forecasting period.

I plan to do a combination forecast for real estate cycle prediction. As you can see above I read a lot of literature about it, but cannot yet decide, which models I choose to implement in R?

Any recommendation, on which factors a combination forecast can be decided?

I appreciate your replies!