In a linear model, it's easy to assess the importance of each explanatory variable. If the assumptions of the model are met, given two explanatory variables $x_1$ and $x_2$, both with a regression coefficient significantly different from zero, $x_1$ would be more important than $x_2$ if its estimated regression coefficient $\hat\beta_1$ is bigger than the estimated regression coefficient $\hat\beta_2$ of $x_2$. In other words, $x_1$ has a stronger association with the response than $x_2$ if $\hat\beta_1>\hat\beta_2$.

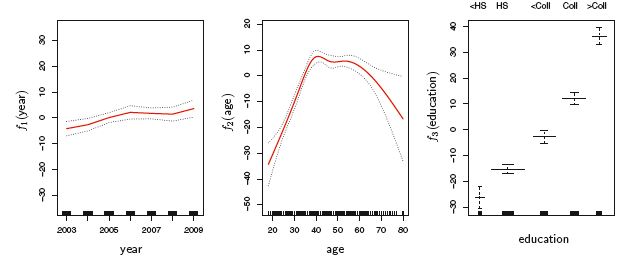

I was wondering if it's possible to assess the importance of the explanatory variables in a generalized additive model as well. The output of a GAM consists in the graphs of the estimated function for each variable. For instance:

I was wondering if it is possible to assess variable importance by looking at the values of the y-axis of each of this plots. Suppose that 'year', 'age' and 'education' are all significant and that the assumptions of the model are met.

Since the codomain of $\hat f_1(year)$ is approximately $[-10,10]$ while the codomain of $\hat f_2(age)$ is about $[-40,10]$, can I conclude that 'age' is more important than 'year'?

In other words, can I conclude that 'age' has a stronger association with the response than 'year'?

Doesn't $\hat f_1(year)$ translate vertically as 'age' varies? Does this affect interpretation and the assessment of variable importance?