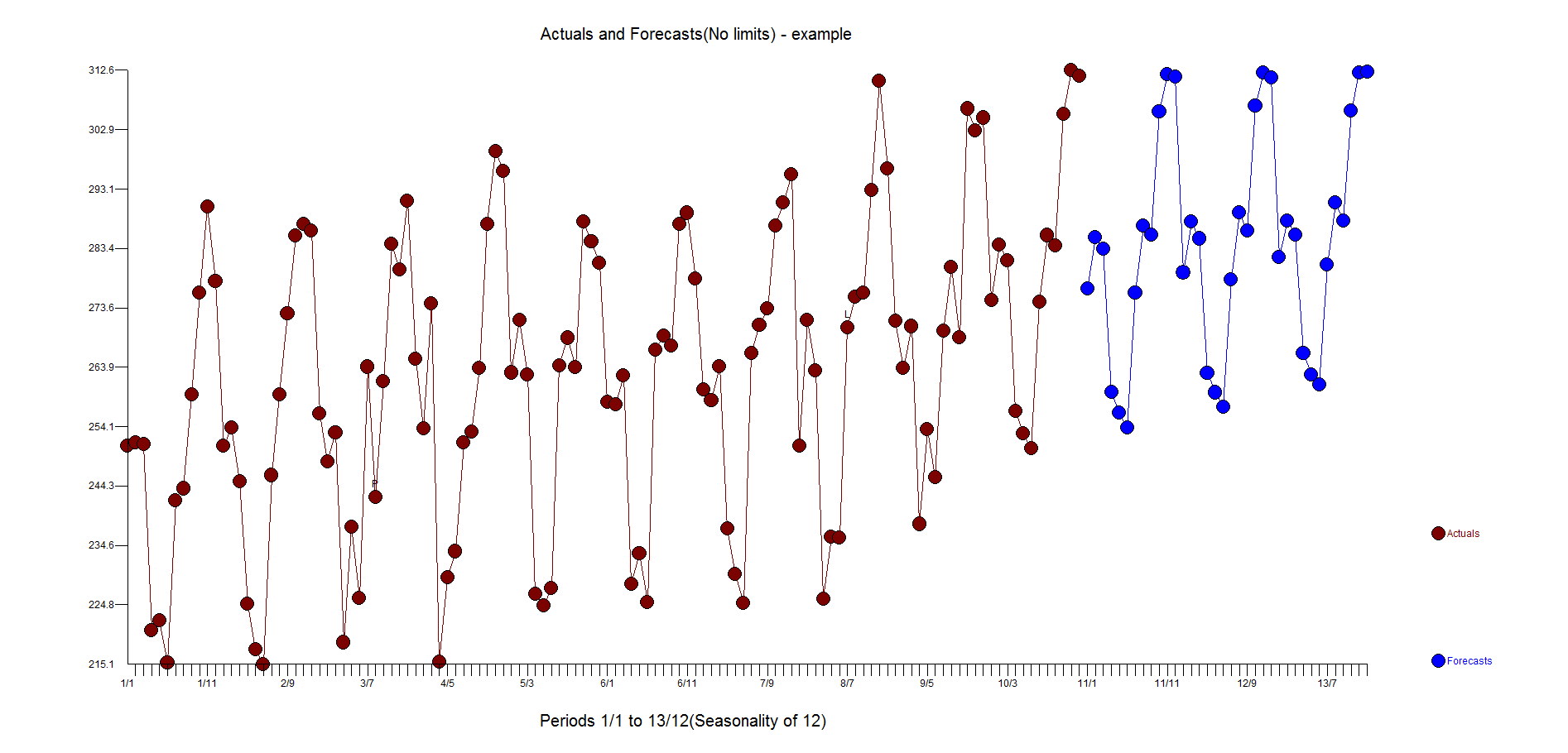

I have a 10 years daily data series, with no indicative trend on the first 8 years but seemingly exponential growth in the last 2.

I’m using R with forecast package.

auto.arima recommends:

ARIMA(0,0,2)SARIMA(2,1,0,)[12]+drift=0.25

Note that no first difference is recommended. I worry that my future forecast (using this model) will not fairly account for the exponential growth witnessed for the past 2 years, since the drift=0.25 is an under representation of trend? Is my worry unfounded because differencing effectively remove trend. Otherwise please advise what can I do about it?

It’s not a structural break, but perhaps a “time varying parameter” (according to Prof. Rob Hyndman – but how can I do that? http://robjhyndman.com/hyndsight/structural-breaks/ – any easy solutions/references to this?) P.s. I could only answer this question if my mathematics is good enough…thanks in advance.