Any general material on how to update with multivariate normal priors would do., such as text book chatpers or paper, notes etc. I tried to google, nothing similar/relevant was found.

I read this in a paper(Erdem 1998) but could not understand how they derive the posterior upto to time T. No idea how to type equations here so i used a screen shot for my questions.

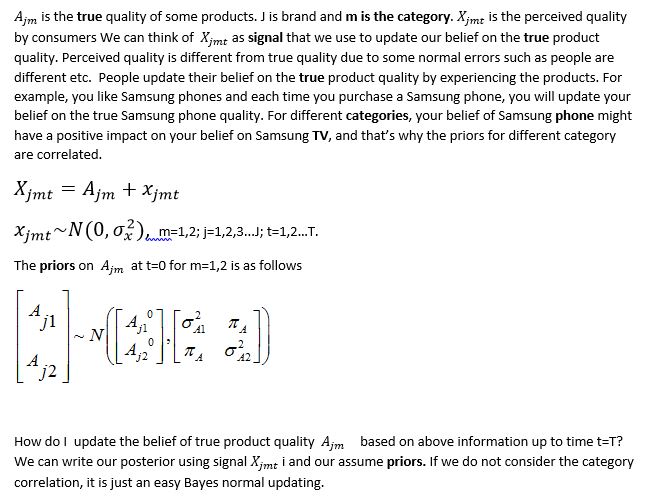

Some background information. The key assumption here is consumers does have a perfect perceptions of the TRUE quality of a product (brand quality etc.). But the true product quality is fixed in perspective of the company. The consumer’s perceived quality is different from true quality but depend on the true quality. Each time they purchase, they update their belief on the true quality (or mean quality). The consumers evaluate the product quality as a Bayesian.