Returning to the discarded HMM approach. An HMM is just a state space model that assumes discrete hidden state. I think you have dismissed the state space approach too soon.

The forecasting question you bring up is quite general for such models which I'll discuss in discrete time formulation, since that's what you've got. (If you happen to know about how Kalman filters work, use that intuition; they're used for very similar state space models when gaussian assumptions apply.)

State and the role of past observations

The basic assumption of any state space model is that the future is independent of the past given the current (hidden) state, and that the observations at a point depend only on the hidden state. Consequently when you have the state you don't need the preceding observed values or states. (And if that isn't enough, you need a formulation with more state...) The state is intended to represent all the relevant information.

Forecasting

Conceptually speaking, to forecast, you start with a distribution over the current hidden state, and you use the estimated transition function -- a transition matrix in the HMM case -- to propagate this distribution forward in time. Once you've moved forward to the point in time where you want to forecast you have a (wider) distribution over the future state. (Alternatively in the HMM case you can find the most likely state to be in then, but you will have neglected quite a bit of uncertainty.) You then generate a predictive distribution over observables by taking a weighted average of the conditional distribution of the observations where the weights are from the distribution over the hidden state.

Basically it's just like filtering, only without tightening up the state estimate on the basis of observations. On cursory glance, the packages you mention don't seem to have a function for more than one step ahead forecasting (because that's needed to compute the likelihood) but now you know what you want to do, you may be able to persuade them to do so, or write the relevant function yourself.

This is described in mathematical detail in a bunch of places, e.g ch. 5 of Zucchini and MacDonald (2008) for the HMM case. They also offer an R implementation. Petris and Patrone (2011) is a more general review of state space model packages in R, including those that work with non-discrete state models. These would be good places to start.

Multivariate state space modelling is not particularly straightforward, but most of the difficulties are numerical and good implementations for the classic models are increasingly available.

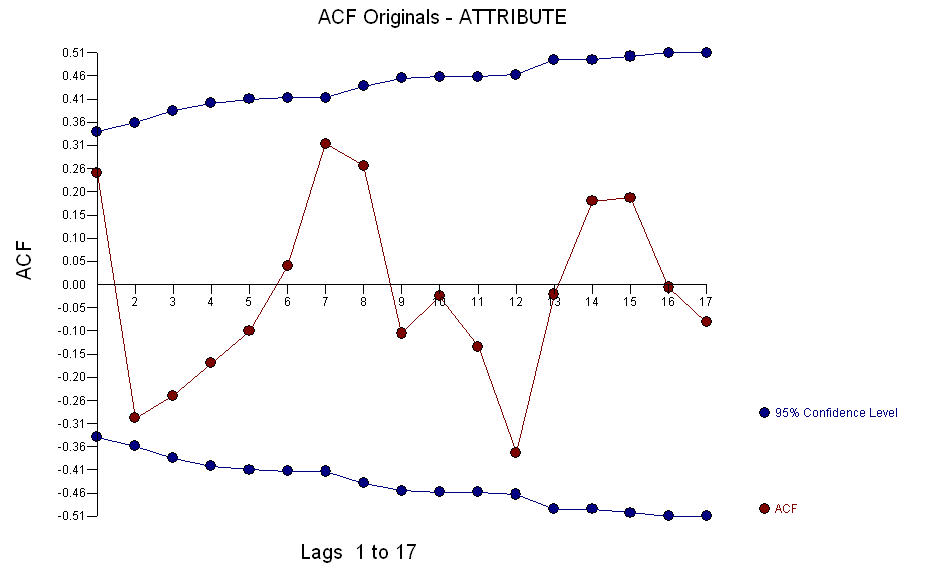

and the ACF of the data

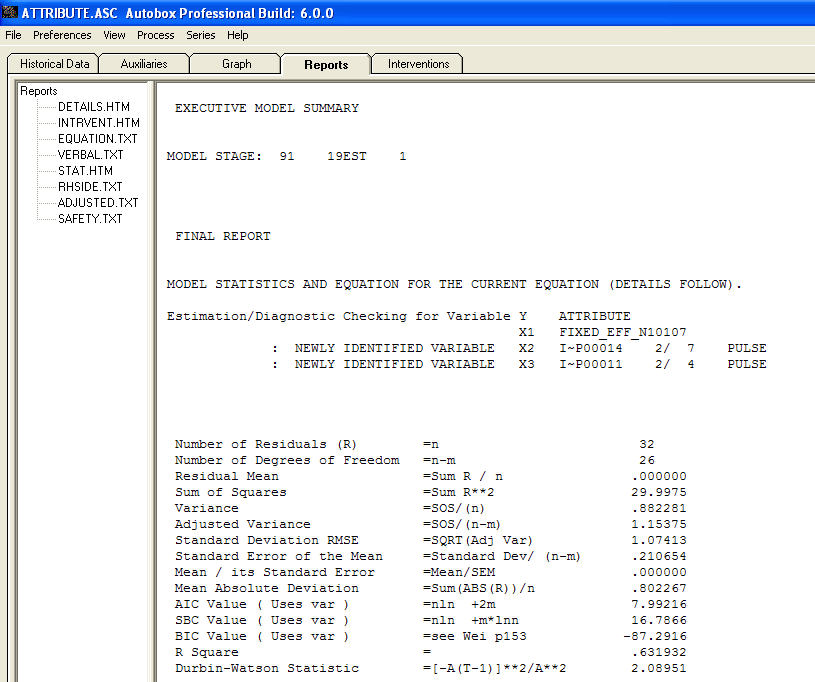

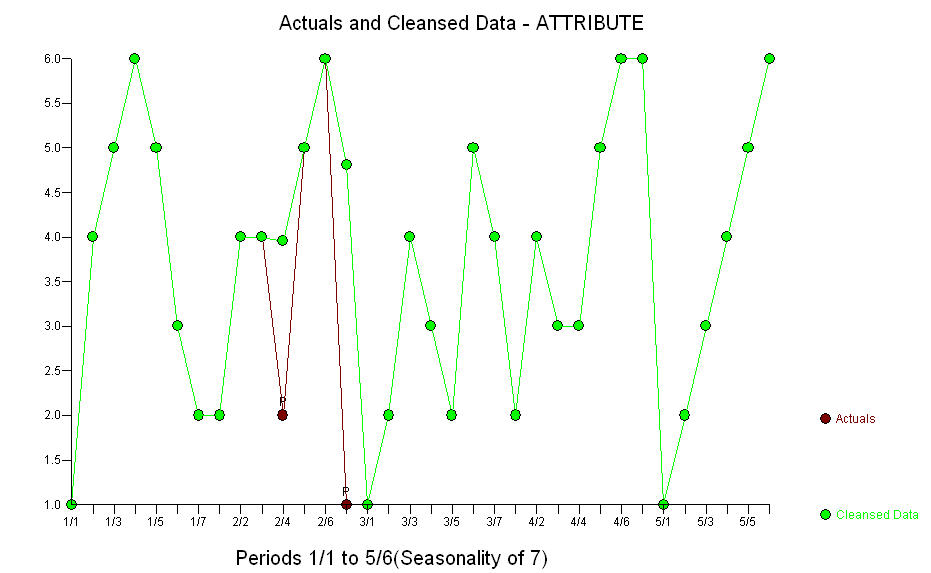

and the ACF of the data  suggest that the data might be daily as the ACF of lag 7 suggests structure. A model was automatically developed which developed an auto-regressive memory of order 2 and an indicator variable for day 1 of each week with two Pulses ( anomalies) being identified at periods 14 and period 11

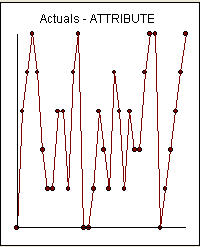

suggest that the data might be daily as the ACF of lag 7 suggests structure. A model was automatically developed which developed an auto-regressive memory of order 2 and an indicator variable for day 1 of each week with two Pulses ( anomalies) being identified at periods 14 and period 11  . The Actual and Cleansed plot illuminate the two unusual data points .

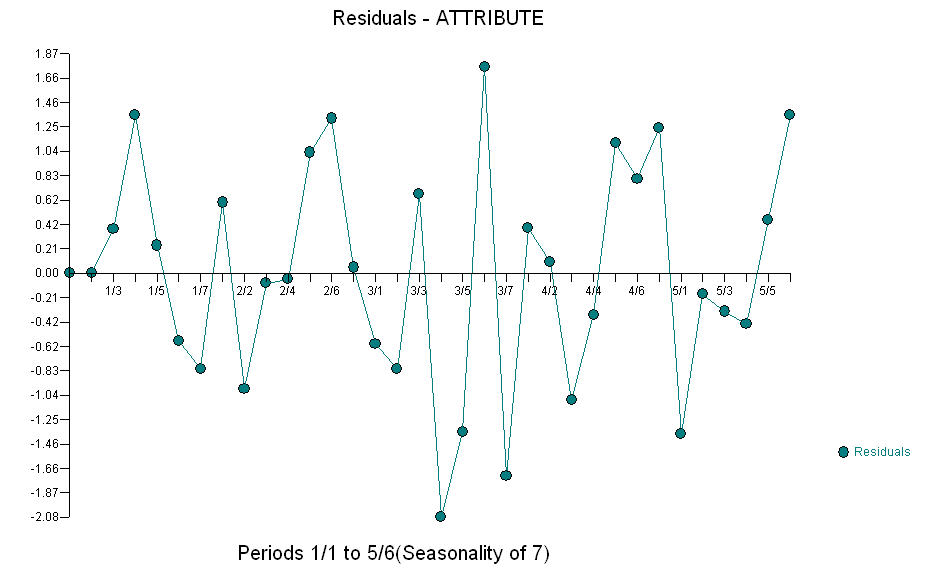

. The Actual and Cleansed plot illuminate the two unusual data points . . The residuals from the model appear visually to be "random"

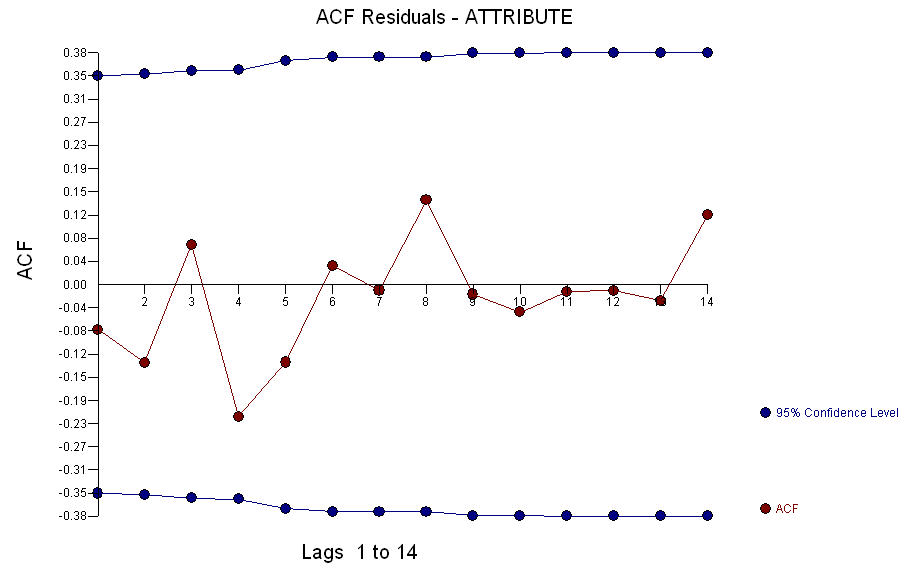

. The residuals from the model appear visually to be "random"  and the ACF of the Residuals appears to support that conclusion

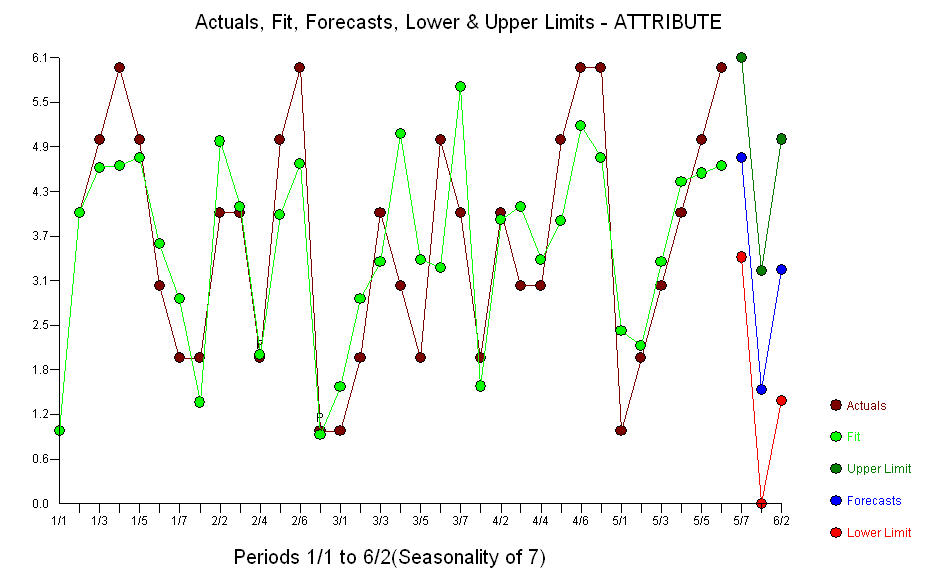

and the ACF of the Residuals appears to support that conclusion  . The actual/fit/forecast plot is shown here

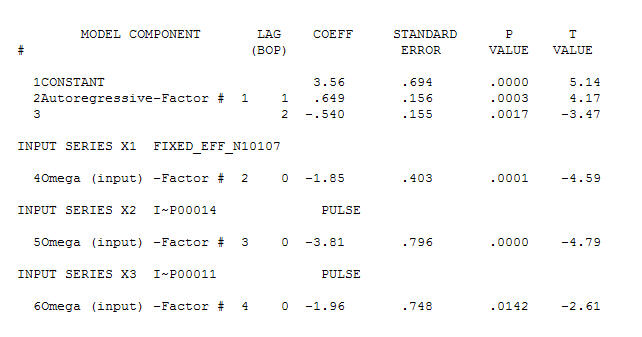

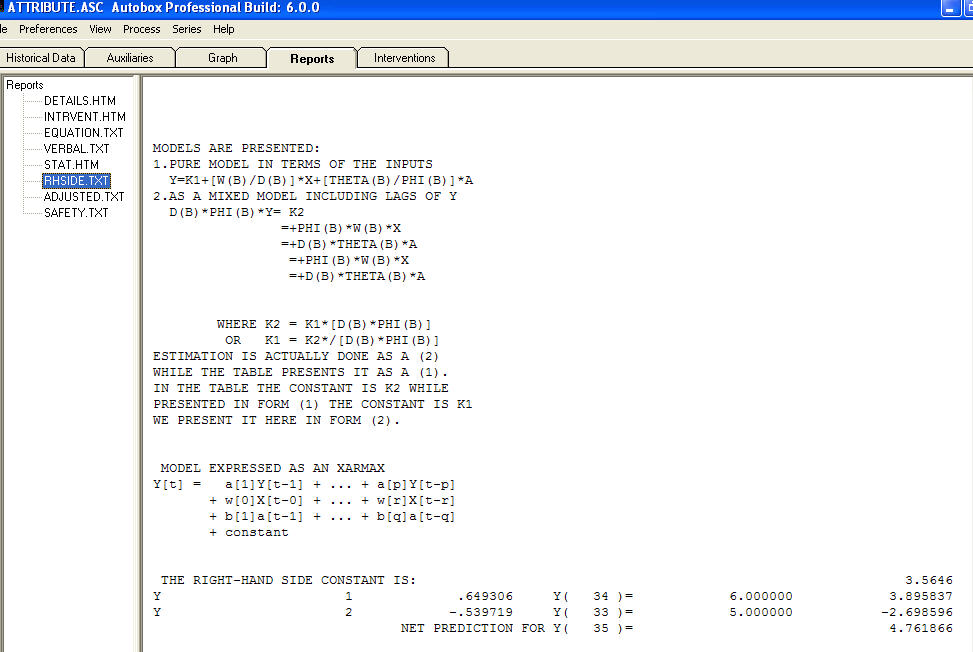

. The actual/fit/forecast plot is shown here . This model can be expressed as Pure Right-Hand Side ala a regression equation

. This model can be expressed as Pure Right-Hand Side ala a regression equation  Note that when predicting the Pulse Indicators play no role as future values of these indicators are expected to be 0 while the future value of the first day of the week will be zero except for the first day of the week. For example if we are predicting out 14 days from period 34 , this would mean 0,1,0,0,0,0,0,1,0,0,0,0,0,0 .Note that all models are wrong but some models are useful ( attributed to G.E.P.Box ) .

Note that when predicting the Pulse Indicators play no role as future values of these indicators are expected to be 0 while the future value of the first day of the week will be zero except for the first day of the week. For example if we are predicting out 14 days from period 34 , this would mean 0,1,0,0,0,0,0,1,0,0,0,0,0,0 .Note that all models are wrong but some models are useful ( attributed to G.E.P.Box ) .