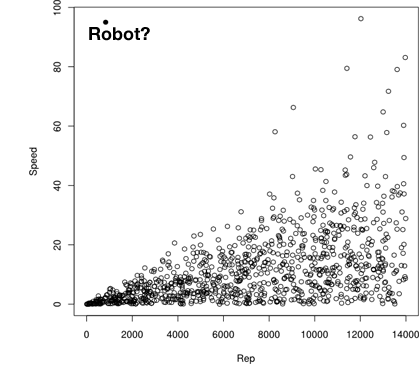

This may be very simple. Consider the following figure, minus the robot. How can I model the standard deviation of Speed as a function of Rep

I can chop the rep up into arbitrary pieces (e.g. 2000 Rep's), calculate the sd, and then draw a regression line between de standard deviations, I also thought about moving window but that doesn't seem right. Is there a better, more continuous way, irrespective of arbitrary binning, to model standard deviation as a function of x?