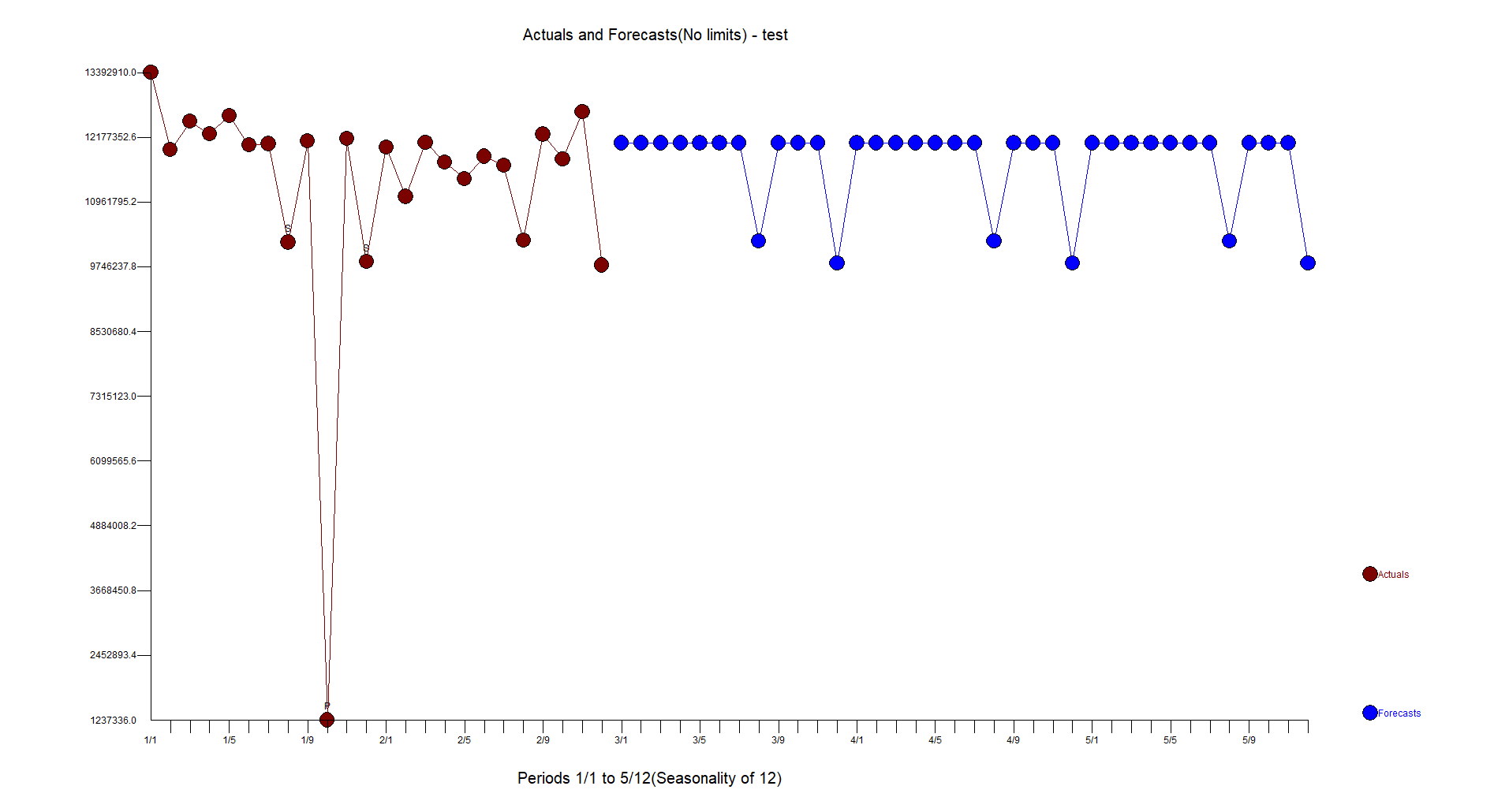

I have a data as follows

Date Paid

Jan-14 13392905

Feb-14 11939873

Mar-14 12473667

Apr-14 12237110

May-14 12579693

Jun-14 12030095

Jul-14 12052101

Aug-14 10205025

Sep-14 12102526

Oct-14 1237336

Nov-14 12148331

Dec-14 9842860

Jan-15 11990085

Feb-15 11061740

Mar-15 12076397

Apr-15 11702514

May-15 11395657

Jun-15 11817594

Jul-15 11643682

Aug-15 10243241

Sep-15 12233001

Oct-15 11769231

Nov-15 12652418

Dec-15 9774333

Jan-16 11888965

Feb-16 11892589

Mar-16 11419517

Apr-16 12143787

May-16 12330387

Jun-16 11929805

Jul-16 11583281

Aug-16 11995557

Sep-16 12646047

Oct-16 12677372

Nov-16 13301244

Dec-16 9915846

Using 2014-2015 information I want to generate forecasts until 2020.Hence, I have split the data into train & test

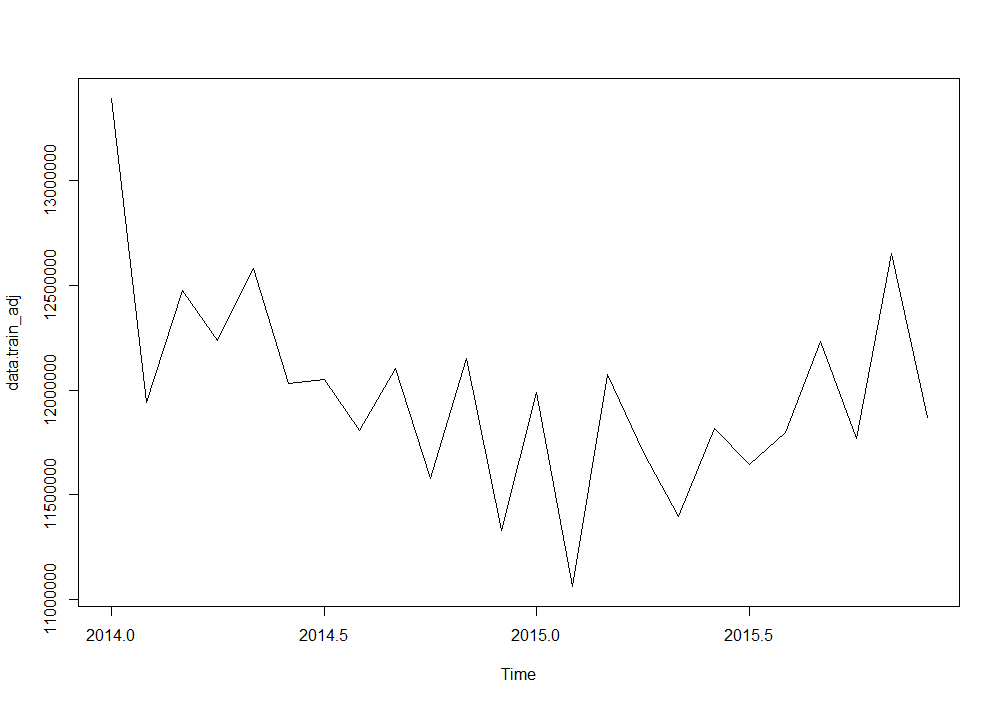

data.train<-window(mydata_ts,start=c(2014,1),end=c(2015,12))

data.test<-window(mydata_ts,start=c(2016,1))

auto.arima(data.train,trace=TRUE,test="kpss",ic="aic")

& following are the results:

Best model: ARIMA(0,0,0) with non-zero mean

Series: data.train

ARIMA(0,0,0) with non-zero mean

Coefficients:

mean

11275058.9

s.e. 463612.8

sigma^2 estimated as 5.381e+12: log likelihood=-385.31

AIC=774.62 AICc=775.19 BIC=776.98

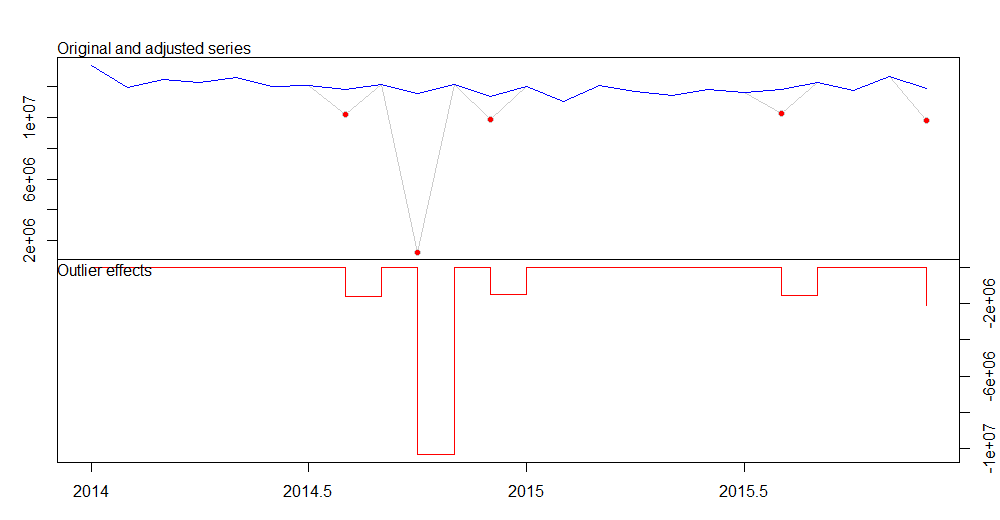

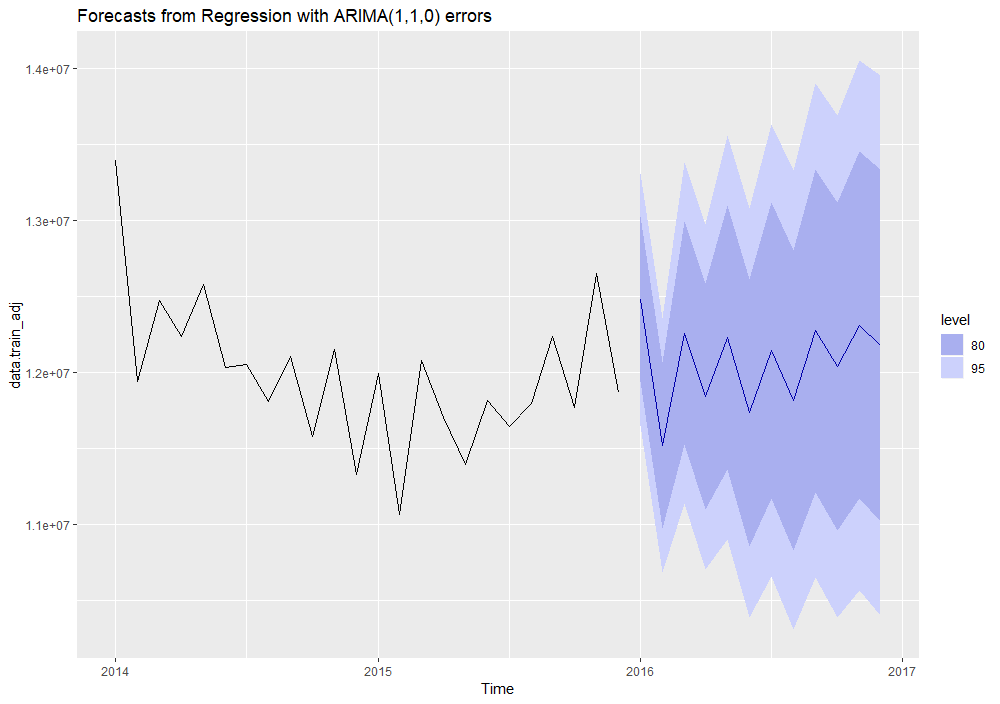

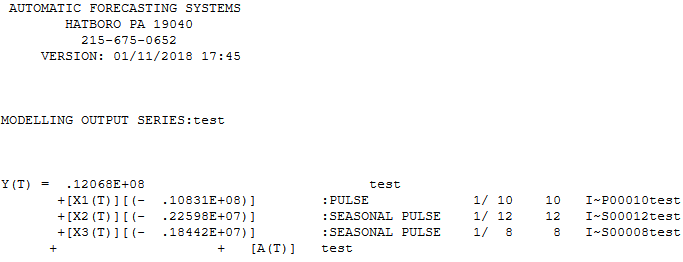

& I get flat forecasts.I have tried using drift but that only helps when forecasting for 2016 & flattens 2017 onward. Is there something that can be done to overcome this.I have also tried the similar exercise in SAS using proc UCM & that seems to generate forecasts better than the auto.arima.

Can someone help out?