In short, there is no such thing as Multivariate Time Series data. The only classic data types out there are: Cross Sections, Time Series, Pooled Cross Sections, and Panel data.

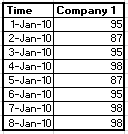

Panel data is multidimensional. Time series is one-dimensional. Time Series data is a type of panel data. Daily closing prices for last one year for 1 company is a Time Series dataset because the time variable alone uniquely identifies each observation. I will work with only 8 days worth of prices instead of a year, but the idea is the same.

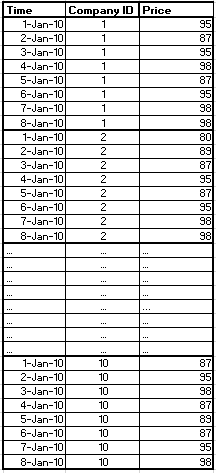

Daily closing prices for last one year for 10 companies can be both a Panel dataset and a Time Series dataset, depending on whether it is in wide or long format.

If the data is organized so that Time still uniquely identifies each observation (i.e. wide format) then it is still a time series dataset, and you will have different columns for the daily closing price for each of the 10 companies. See example below:

If, on the other hand, it is organized so that Time alone no longer uniquely identifies each observation (i.e. long format) then it is a panel dataset. With 10 companies, you need to use Time and Company ID together to uniquely identify each observation. See example below:

In any statistical software it is straightforward to reshape a dataset from wide to long and from long to wide.

The term Multivariate Time Series is heard around, but it refers not to a type of dataset but to a type of analysis. To be more exact, it refers to the type of time series regression analysis in which there is more than one response variable. (Make sure to distinguish it from Multiple Time Series regression, which refers to a regression with one response variable and several predictor variables). One example of Multivariate Time Series Analysis is VAR (Vector AutoRegression).

More on VAR here:

https://en.wikipedia.org/wiki/Vector_autoregression

I hope this helps.