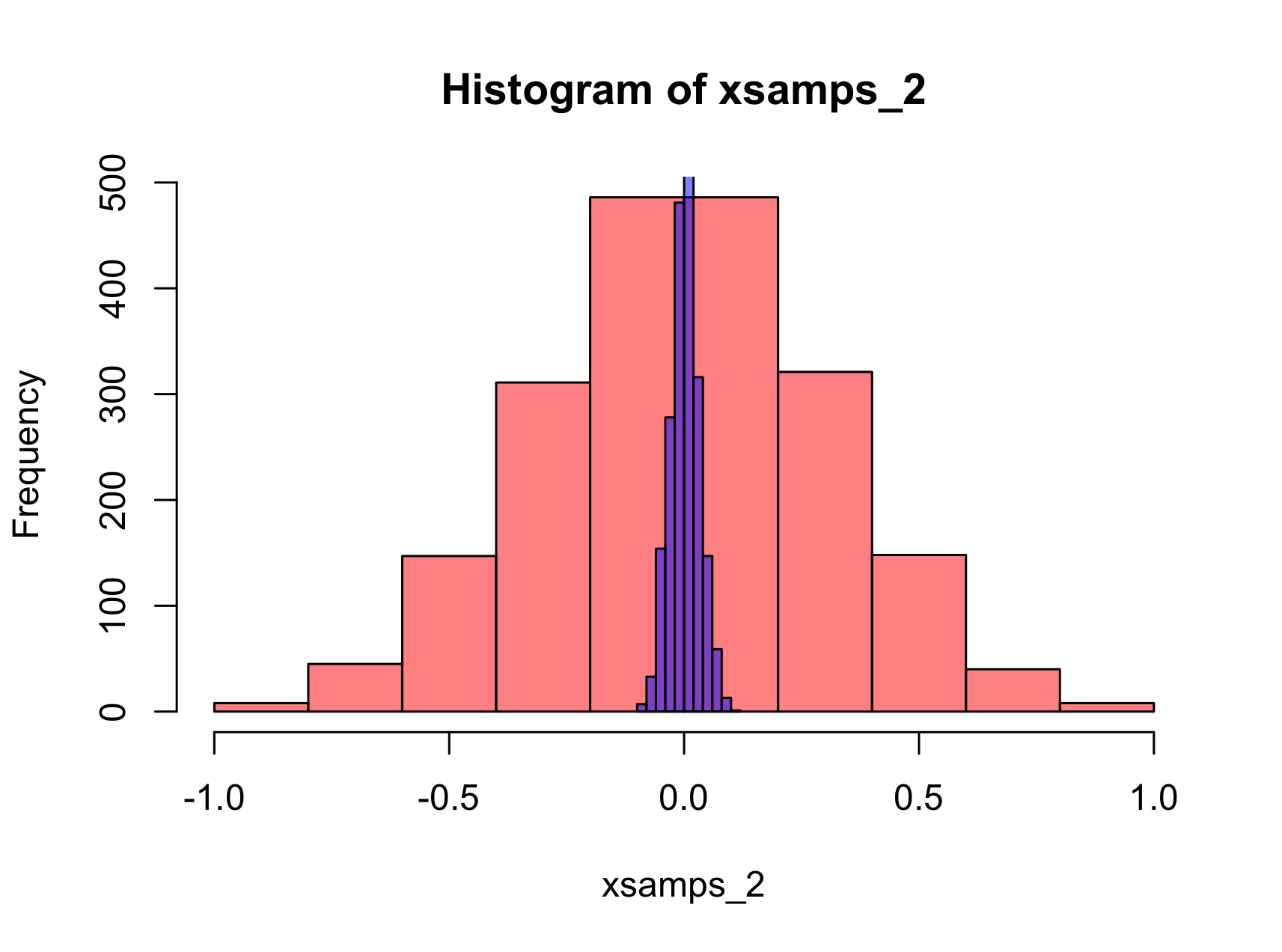

Let $\{X_1,X_2,\dots,X_n\}$ be a sample of $n$ iid observations of a random variable $X$, and let $\overline X_n = \frac{1}{n} \sum_{i=1}^n X_i$ be the sample mean.

Now suppose we want to use bootstrapping to estimate, for example, the variance of the sample mean. Let $\{X_1^{*(i)},X_2^{*(i)},\dots,X_n^{*(i)}\}$ be a sample with replacement from the original sample and let $\overline X_n^{*(i)} = \frac{1}{n} \sum_{j=1}^n X_j^{*(i)}$ be the sample mean for the $i$-th bootstrap sample.

Let $B$ be the number of bootstrap rounds. Then we have a bootstrap estimate of the variance. $$ \text{Var}_{B,n} = \frac{1}{B-1} \sum_{i=1}^B (\overline X_n^{*(i)} - \overline X_B^*)^2, \quad \quad \text{where} \ \overline X_B^* = \frac{1}{B} \sum_{i=1}^B \overline X_n^{*(i)}. $$

Suppose $n$ is very large and computing the bootstrap variance estimate will be computationally intensive. For example suppose we were using a slow computer and take $n=10^7$

To speed things up, we decide that instead of repeatedly drawing samples of size $n$ we will instead draw samples of size $m \ll n$ with replacement. For example, for $n=10^7$, we could take $m=5000$.

Let $\{Y_1^{*(i)},Y_2^{*(i)},\dots,Y_m^{*(i)}\}$ be a sample with replacement from the original sample $\{X_1,X_2,\dots,X_n\}$ and let $\overline Y_m^{*(i)} = \frac{1}{m} \sum_{j=1}^m Y_j^{*(i)}$ be the sample mean for the $i$-th bootstrap sample.

Now, this time we have the variance estimate: $$ \text{Var}_{B,m} = \frac{1}{B-1} \sum_{i=1}^B (\overline Y_m^{*(i)} - \overline Y_B^*)^2, \quad \quad \text{where} \ \overline Y_B^* = \frac{1}{B} \sum_{i=1}^B \overline Y_m^{*(i)}. $$

Is $\text{Var}_{B,m}$ a valid estimate of the variance of the sample mean? One issue that I have noticed is that since $m$ is such so much smaller than $n$ that we have effectively sampled without replacement when we computed $\text{Var}_{B,m}$. Is this a problem?