The key point is that parameter estimates are random variables. If you sample from a population many times and fit a model each time, then you get different parameter estimates. So it makes sense to discuss the expectation and the variance of these parameter estimates.

Your parameter estimates are "unbiased" if their expectation is equal to their true value. But they can still have a low or a high variance. This is different from whether the parameter estimates from a model fitted to a particular sample are close to the true values!

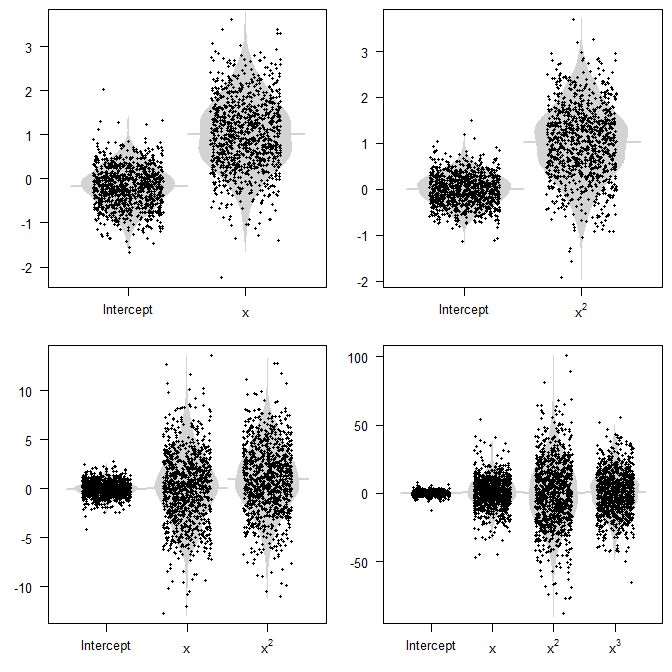

As an example, you could assume a predictor $x$ that is uniformly distributed on some interval, say $[0,1]$, and $y=x^2+\epsilon$. We can now fit different models, let's look at four:

- If we regress $y$ on $x$, then the parameter will be biased, because its parameter will have an expected value greater than zero. (And of course, we don't have a parameter for the $x^2$ term, so this inexistent parameter could be said to be a constant zero, which is also different from the true value of $1$.)

- If we regress $y$ on $x^2$ alone, our model is the true data generating process (DGP). Our parameter estimate will be unbiased and have minimum variance.

- If we regress $y$ on $x$ and $x^2$, then we have the true DGP, but we also have a superfluous predictor $x$. Our parameter estimates will be unbiased (expectations $0$ for the intercept and the $x$ coefficient, $1$ for the $x^2$ one), but they will have a higher variance.

- Finally, if we regress $y$ on $x$, $x^2$ and $x^3$, the same holds: we have unbiased parameter estimates, but with an even larger variance.

Below are parameter estimates from 1000 simulations (R code at the bottom). Note how the point clouds cluster around the true value (or not), but also how spread out they are.

The conceptual problem is that we usually don't see these random variables. All we see is a single sample from our population, and a single model, and a single realization of our parameter estimates. This will be one of the dots in the plot. The key thing to keep in mind is that if our model is misspecified, then variances will be larger. And of course, if we have large variances, then our model can easily be very far away from the true DGP, and be very misleading, whether we do inference or prediction.

R code:

n_sims <- 1e3

n_sample <- 20

param_estimates <- list()

param_estimates[[1]] <- matrix(nrow=n_sims,ncol=2)

param_estimates[[2]] <- matrix(nrow=n_sims,ncol=2)

param_estimates[[3]] <- matrix(nrow=n_sims,ncol=3)

param_estimates[[4]] <- matrix(nrow=n_sims,ncol=4)

for ( ii in 1:n_sims ) {

set.seed(ii) # for reproducibility

xx <- runif(n_sample,0,1)

yy <- xx^2+rnorm(n_sample)

param_estimates[[1]][ii,] <- summary(lm(yy~xx))$coefficients[,1]

param_estimates[[2]][ii,] <- summary(lm(yy~I(xx^2)))$coefficients[,1]

param_estimates[[3]][ii,] <- summary(lm(yy~xx+I(xx^2)))$coefficients[,1]

param_estimates[[4]][ii,] <- summary(lm(yy~xx+I(xx^2)+I(xx^3)))$coefficients[,1]

}

beeswarm_matrix <- function(MM, amount=0.3, add.boxplot=FALSE, add.beanplot=FALSE, names=NULL, pt.col=NULL, ...) {

# beeswarm plots of matrix columns

plot(c(1-2*amount,ncol(MM)+2*amount),range(MM,na.rm=TRUE),xaxt="n",type="n",...)

axis(1,at=1:ncol(MM),labels=if(is.null(names)){colnames(MM)}else{names},...)

if ( add.boxplot ) boxplot(MM, add=TRUE, xaxt="n", outline=FALSE, border="grey", ...)

if ( add.beanplot ) {

require(beanplot)

sapply(1:ncol(MM),function(xx)beanplot(MM[,xx],add=TRUE,what=c(0,1,1,0),xaxt="n",

col=c(rep("lightgray",3),"lightgray"),border=NA, at=xx,...))

}

pt.col.mat <- matrix(if(is.null(pt.col)){"black"}else{pt.col},nrow=nrow(MM),ncol=ncol(MM),byrow=TRUE)

points(jitter(matrix(1:ncol(MM),nrow=nrow(MM),ncol=ncol(MM),byrow=TRUE),amount=amount),MM,col=pt.col.mat,...)

}

opar <- par(las=1,mfrow=c(2,2),mai=c(.5,.5,.1,.1),pch=19)

beeswarm_matrix(param_estimates[[1]],add.beanplot=TRUE,xlab="",ylab="",cex=0.5,

names=c("Intercept",expression(x)))

beeswarm_matrix(param_estimates[[2]],add.beanplot=TRUE,xlab="",ylab="",cex=0.5,

names=c("Intercept",expression(x^2)))

beeswarm_matrix(param_estimates[[3]],add.beanplot=TRUE,xlab="",ylab="",cex=0.5,

names=c("Intercept",expression(x),expression(x^2)))

beeswarm_matrix(param_estimates[[4]],add.beanplot=TRUE,xlab="",ylab="",cex=0.5,

names=c("Intercept",expression(x),expression(x^2),expression(x^3)))

par(opar)