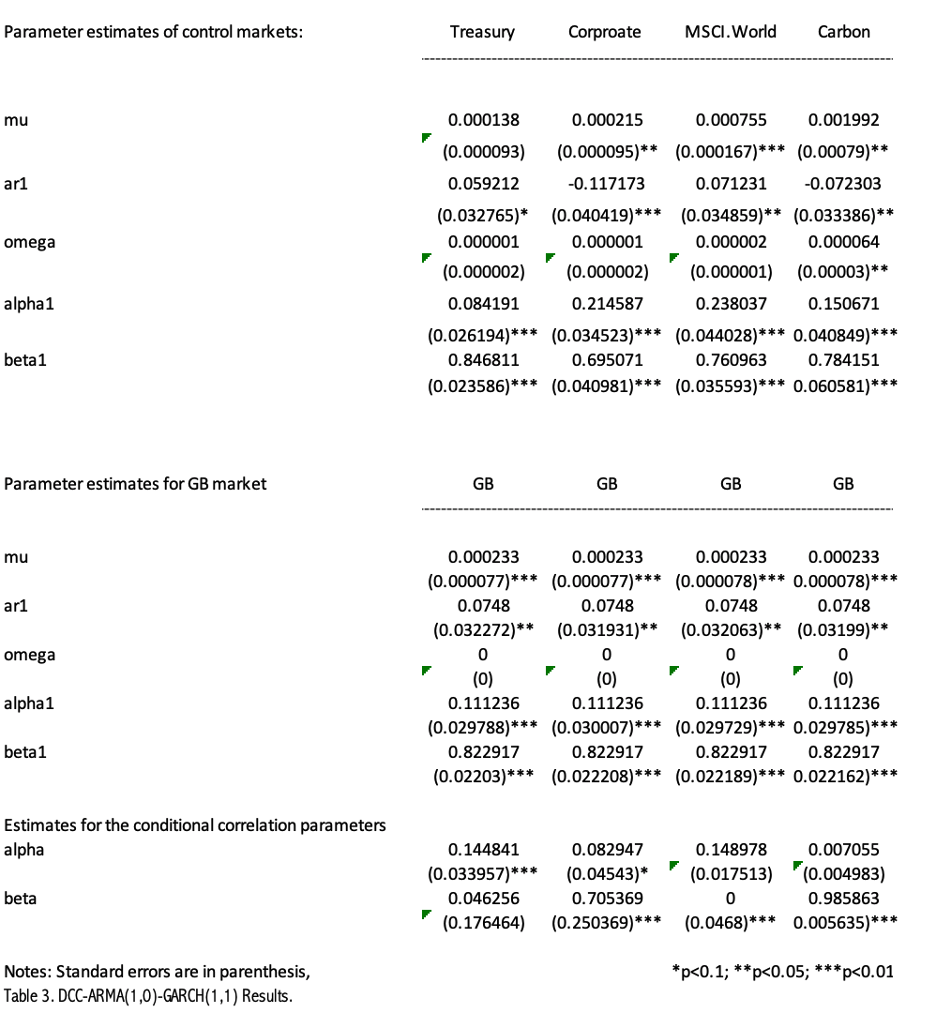

I've used DCC-ARMA(1,0) -GARCH(1,1) to model green bond co-movement with some other marekts. In the output, I get the parameters "dccalpha" and "dccbeta". However, I do not know how to interpret these. Don't know if the output is needed to answer my quesiton but included it in the bottom in case someone is interested.

From previous literature, I have understood that alpha1 and beta1, aka jointalpha and jointbeta, tell me the degree of volatility spillovers in-between the time series. Is this true or does they rather show the correlation of the time series? The reason why I distinguish these two is that “to me” correlation indicates the strength of which two variables tend to co-move which does not have to imply a causal relationship whereas spillovers means that volatility in prices of one market has a causal effect on price movements in another market.

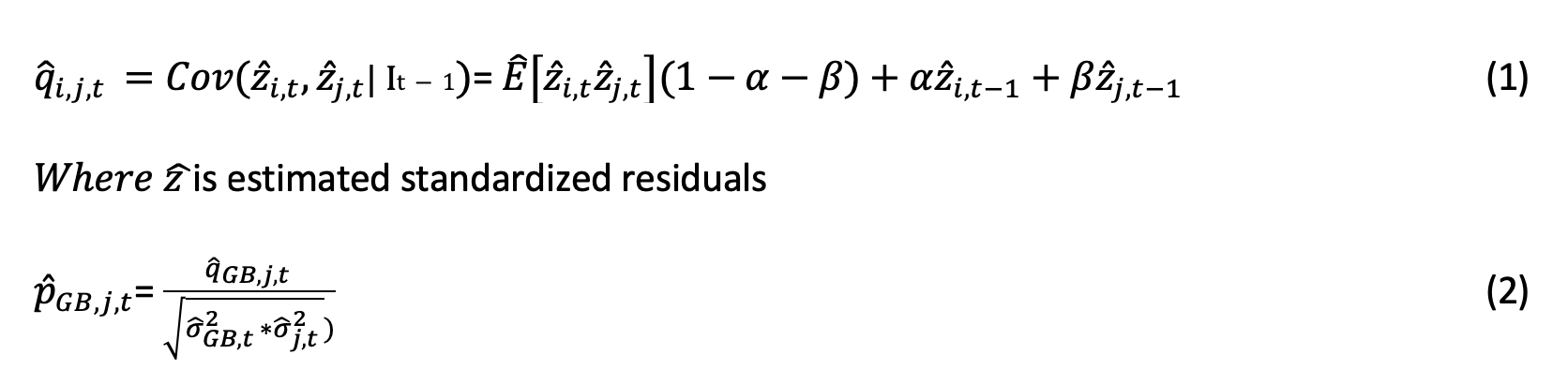

*** Below is an update form the orignially posted question. It was made in order to answer Richard Hardy's response with an equation containing subscripts and denotations. These details makes the formula easier to understand.