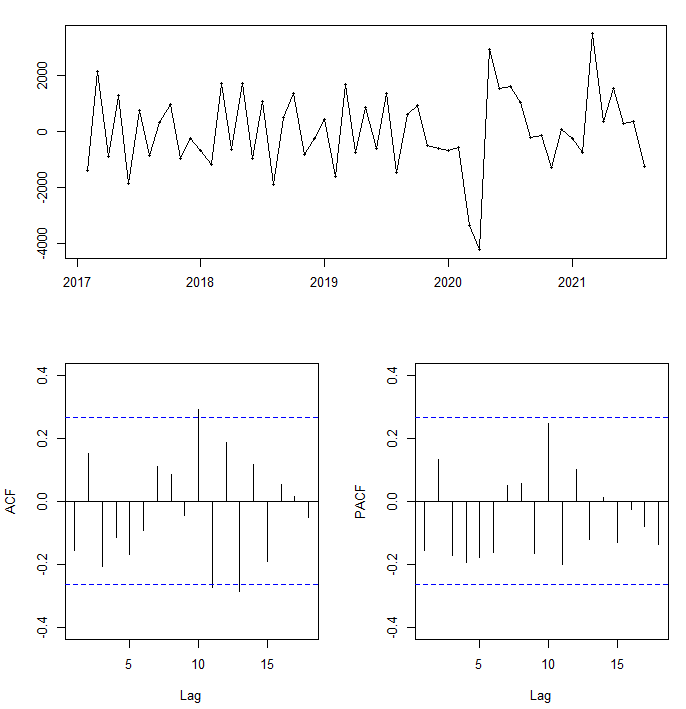

I have been fussing over the ACF and PACF plots with 1 order of differencing (passed the ADF test) but I haven't found any information that deals with ACF and PACF plots that have lags as large as mine or data as irregular as mine.

From Hyndman's textbook I gather that the PACF plot is decaying towards zero and the ACF plot is last significant at lag 13. So would this result in an ARIMA(0,1,13) model?

auto.arima is producing vastly different results and I am confused about what path forward is the right path to take given the unusualness of the time-series.