(Hi, sorry, this is probably a very entry level question for this site. Let me know if something is not OK.)

Let's say that we use the Monte Carlo method to estimate the area of an object, in the exact same way you'd use it to estimate the value of π.

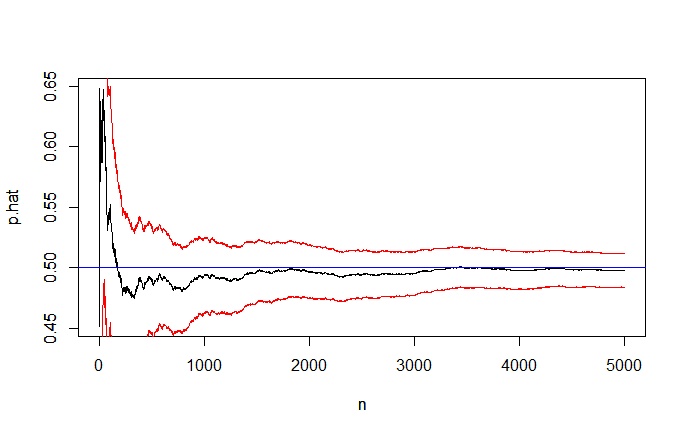

Now, let's say we want to calculate the certainty of our simulation result. We've cast n samples (taken from uniform distribution of the sample area), m of which landed inside the object, so the area of the object is approximately m/n of the total sampled area. We would like to make a statement such as:

"We are 99% certain that the area of the object is between a1 and a2."

How can we calculate a1 and a2 above (given n, m, total area, and the desired certainty)?

I wrote a program which attempts to estimate this bound numerically. Here the samples are points in [0,1), and the object is the segment [0.25,0.75). It prints a1 and a2 for 50%, 90%, and 99%, for a range of sample counts:

import std.algorithm;

import std.random;

import std.range;

import std.stdio;

void main()

{

foreach (numSamples; iota(0, 1000+1, 100).filter!(n => n > 0))

{

auto samples = new double[numSamples];

enum objectStart = 0.25;

enum objectEnd = 0.75;

enum numTotalSamples = 10_000_000;

auto numSizes = numTotalSamples / numSamples;

auto sizes = new double[numSizes];

foreach (ref size; sizes)

{

size_t numHits;

foreach (i; 0 .. numSamples)

{

auto sample = uniform01!double;

if (sample >= objectStart && sample < objectEnd)

numHits++;

}

size = 1.0 / numSamples * numHits;

}

sizes.sort;

writef("%d samples:", numSamples);

foreach (certainty; [50, 90, 99])

{

auto centerDist = numSizes * certainty / 100 / 2;

auto startPos = numSizes / 2 - centerDist;

auto endPos = numSizes / 2 + centerDist;

writef("\t%.5f..%.5f", sizes[startPos], sizes[endPos]);

}

writeln;

}

}

(Run it online.) It outputs:

// 50% 90% 99%

100 samples: 0.47000..0.53000 0.42000..0.58000 0.37000..0.63000

200 samples: 0.47500..0.52500 0.44500..0.56000 0.41000..0.59000

300 samples: 0.48000..0.52000 0.45333..0.54667 0.42667..0.57333

400 samples: 0.48250..0.51750 0.46000..0.54250 0.43500..0.56500

500 samples: 0.48600..0.51600 0.46400..0.53800 0.44200..0.55800

600 samples: 0.48667..0.51333 0.46667..0.53333 0.44833..0.55167

700 samples: 0.48714..0.51286 0.46857..0.53143 0.45000..0.54857

800 samples: 0.48750..0.51250 0.47125..0.53000 0.45375..0.54625

900 samples: 0.48889..0.51111 0.47222..0.52667 0.45778..0.54111

1000 samples: 0.48900..0.51000 0.47400..0.52500 0.45800..0.53900

Is it possible to calculate these numbers directly instead?

(Context: I'd like to add something like "±X.Y GB with 99% certainty" to btdu)