I use the generalized form of the Student's-t distribution: \begin{align*} f(l|\nu ,\mu ,\beta) = \frac{\Gamma (\frac{\nu+1}{2})}{\Gamma (\frac{\nu}{2}) \sqrt{\pi \nu} \beta} \left(1+\frac{1}{\nu}\left(\frac{l - \mu}{\beta}\right)^2 \right)^{\text{$-\frac{1+\nu}{2}$}} \end{align*}

I want to have standardized version, i.e. mean zero and a variance of one. Therefore, I set $\mu=0$ and \begin{align*} \beta=\sqrt{\frac{\nu-2}{\nu}} \end{align*} which ensures, that the variance is equal to one. If I now insert this I get after some derivations \begin{align*} f(l|\nu) =(\pi (\nu-2))^{-\frac{1}{2}}\Gamma \left(\frac{\nu}{2} \right)^{-1} \Gamma \left(\frac{\nu+1}{2} \right) \left(1+\frac{l^2}{\nu-2} \right)^{-\frac{1+\nu}{2}} \end{align*} Now my question is: What is the formula for the kurtosis? Is it still $\frac{6}{\nu-4}$?

E.g. consider these data and the following R code:

pinumber<-3.141592653589793

startvalue<-2

loglikstandardizedt <-function(par){

if(par>0) return(-sum(log((pinumber*(par-2))^(-1/2)*gamma(par/2)^(-1)*gamma((par+1)/2)*(1+standresidsapewma^2/(par-2))^(-(1+par)/2))))

else return(Inf)

}

optim(startvalue, fn=loglikstandardizedt, method="Brent",lower=2,upper=250)

param = optim(startvalue,loglikstandardizedt, method="BFGS")$par

If I look at the plot, to see how good the fit is, I do the following code:

# control output

denstiystandtresid<-function (x) (pinumber*(param-2))^(-1/2)*gamma(param/2)^(-1)*gamma((param+1)/2)*(1+x^2/(param-2))^(-(1+param)/2)

plot(density(standresidsapewma),ylim=c(0,0.8))

curve(denstiystandtresid,col="red",add=TRUE)

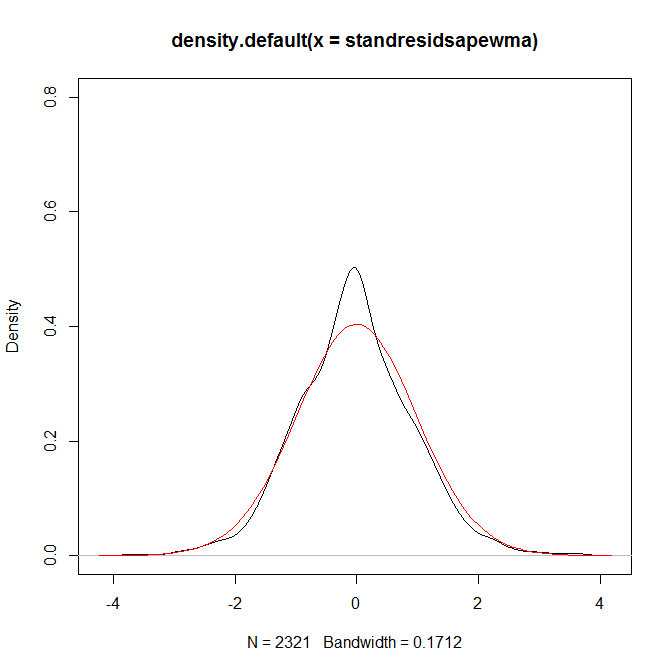

This gives me the following plot:

As you can see, the fit is, let's say fairly ok. Now, I am interested in the excess kurtosis. The data has the excess kurtosis of

kurtosis(standresidsapewma)

which gives 0.6470055

I would expect, since the fit is quite ok in the tails, that the fitted distribution has almost the same excess kurtosis, but if I calculated it via the following way (the estimate output for $\nu$ is 8.85009):

$\frac{6}{\nu-4}=\frac{6}{8.85009-4}=1.23709$?

which is pretty much more than 0.64. This seems to be wrong to me, since I believe, that the fit in the tail is quite ok, so the kurtosis should be almost the same? Is my formula for calculating the ex kurtosis in case of a standardized Student's-t distribution wrong? Or what is my mistake?