I have found an article about stationarity: Variance of a stationary AR(2) model

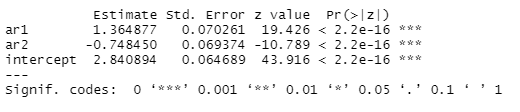

and I have also estimated a model:

And I am not sure if I have understood it, is it truly stationary? And if so, could you show me how to derive it analytically?

I have found an article about stationarity: Variance of a stationary AR(2) model

and I have also estimated a model:

And I am not sure if I have understood it, is it truly stationary? And if so, could you show me how to derive it analytically?

You can write the process in companion form (as a VAR(1)): $$\left[ \begin{array}{c} x_{n} \\ x_{n-1}% \end{array}% \right] =\left[ \begin{array}{c} 2.84 \\ 0% \end{array}% \right] +\left[ \begin{array}{cc} 1.36 & -0.75 \\ 1 & 0% \end{array}% \right] \left[ \begin{array}{c} x_{n-1} \\ x_{n-2}% \end{array}% \right] +\left[ \begin{array}{c} \varepsilon _{n} \\ 0% \end{array}% \right] $$ The eigenvalues of the autoregression matrix are within the unit circle. Therefore, the process is stationary.