Can anyone help with the set up of a multiple variable regression function that does not have an intercept (no beta hat 0)? I've tried to figure it out based on class notes for one variable regression without an intercept and multiple variable regression with an intercept but my answers seem way way off.

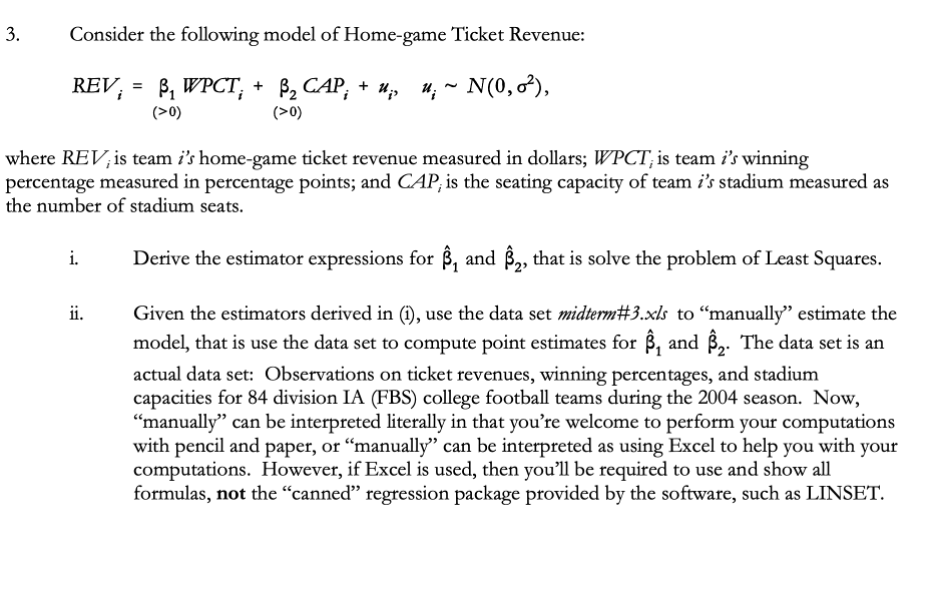

This is the specific question: