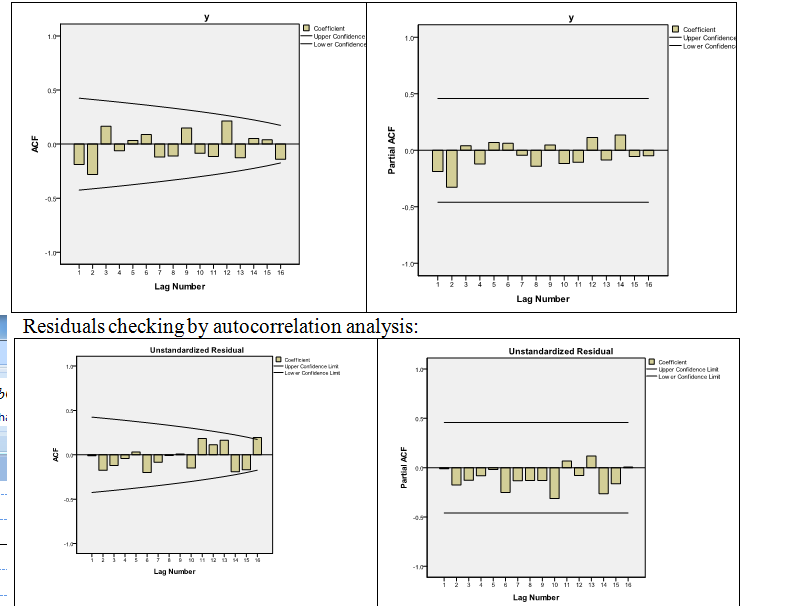

I am learning about ACF and PACF graphs. I am not sure I understand how to interpret the one I got for my data.

I have searched google for some ACF and PACF examples, and I found some samples of different processes, however, the one I am getting doesn't look similar to any. Does this means there is no seasonality, trend and other processes?

I have also created graphs for unstandardized residuals of my model, do not understand what those means? Does it somehow relate to white noise?