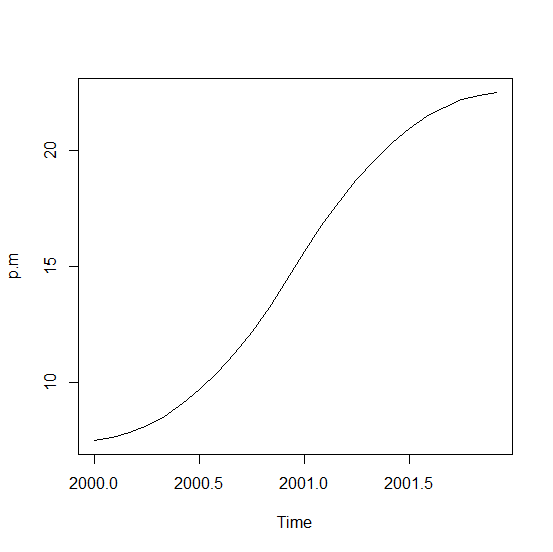

As explained in the title, I would like to transform a yearly dataset into a monthly one, but including a constraint. My current dataset gives the yearly production of a commodity, and from year to year, the production can vary a lot. Let's assume that the yearly production in year X=120, and the yearly production in year X+1=240 If I choose to divide by 12 the total production of year X and X+1 to get the monthly production, there is a gap between December X(=10) and January X+1(=20). I used a Kernel method in order to artificially smooth this gap,and I obtain something like: November X=10, december X=12.5, January X+1=17.5 and February X+1=20 But the problem is that if I sum the production of every month of year X obtained with the Kernel method, it differs from the actual yearly production. The total early production being the only reliable data, it's a problem.

So, to be more specific, my question would rather be the following: is there a statistical method that can "smooth" this kind of dataset, but that can allow for constraint on yearly production?

I apologize if my question is not clear enough. I also apologize to the statistician that may see this post: trying to increase the size of a dataset this way is certainly not a good idea.

I tried a Kernel, but it does not satisfy the yearly production constraint