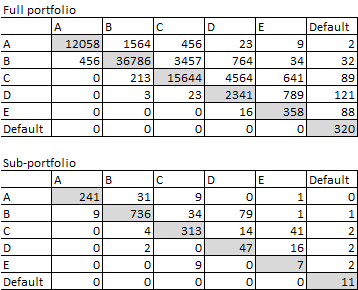

I have a dataset containing observations at time t and t+1 of ratings A (best) to E (worst) and Default. I want to use transition matrices to predict future ratings t+2, t+3, etc

The transition matrix of the full portfolio is monotonic (transition to a further state is less probable than a transition to a nearer state). However, some sub-portfolios are quite small and therefore not monotonic. This is only due to their size and not a pattern of behavior. All ratings are theoretically possible. Default is an absorbing state. How can I smooth the matrices? Preferably with an R package as I'm not a mathematician :-)