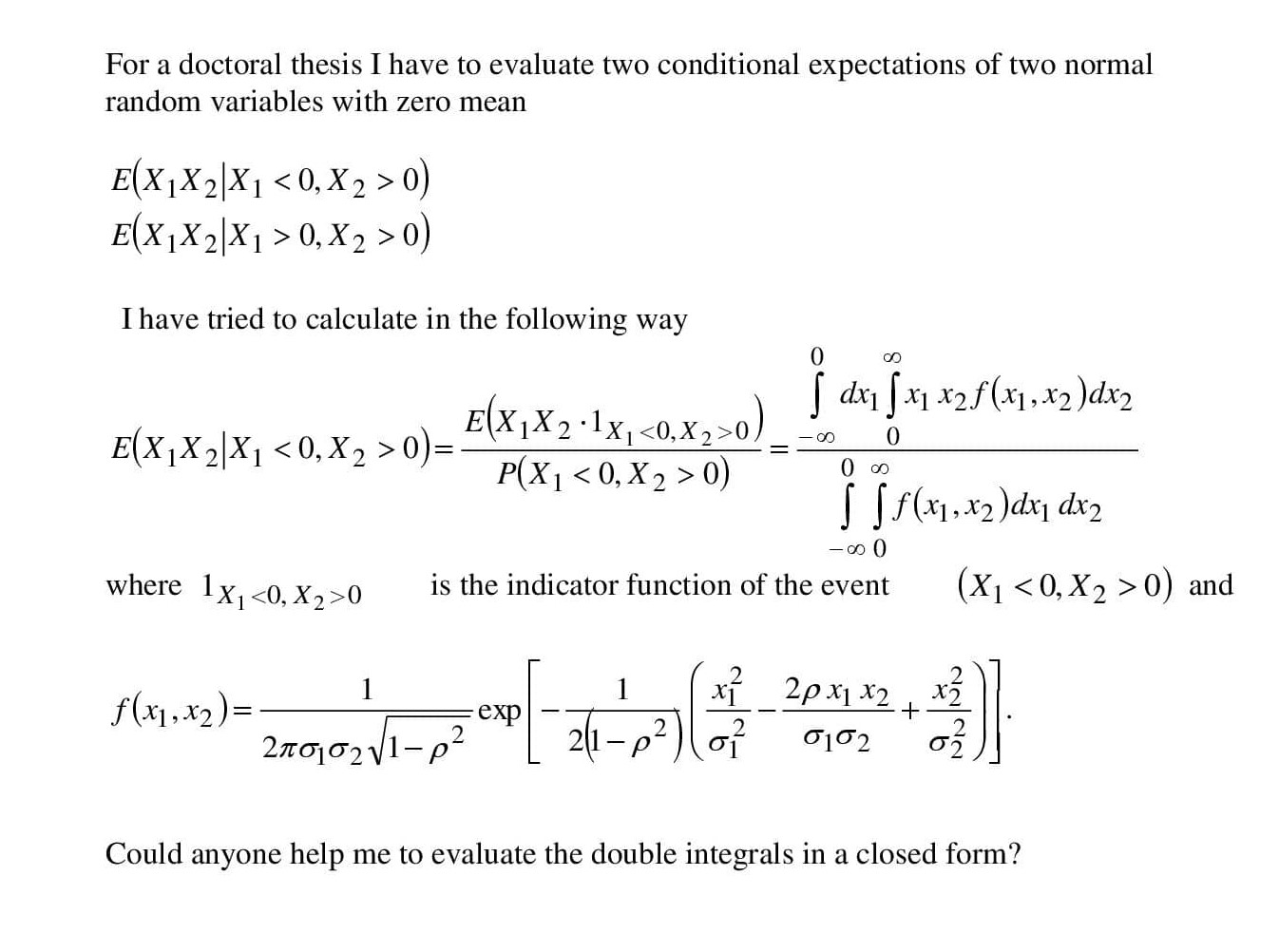

The evaluation of the moments of doubly truncated bivariate normal distribution leads to the formulas with a great complexity. It has not been possible to derive explicit formulae for the moments except some particular cases.

The evaluation of the moments of doubly truncated bivariate normal distribution leads to the formulas with a great complexity. It has not been possible to derive explicit formulae for the moments except some particular cases.

To be explicit, write $f(x_1,x_2,\rho,\sigma_1,\sigma_2)$ for the bivariate normal density.

From the analysis at https://stats.stackexchange.com/a/71303/919 it is clear that the normalizing integral is the angle (as a fraction of the full circle) subtended by the quadrant in question when the ellipse is transformed back to the unit circle; in particular,

$$F(\rho,\sigma_1,\sigma_2) = \iint_{x_1\gt 0,\, x_2\gt 0} f(x_1,x_2,\rho,\sigma_1,\sigma_2)\,\mathrm dx_1\mathrm dx_2 = \frac{1}{\pi} \arctan\left(\sqrt{\frac{1+\rho}{1-\rho}}\right).$$

(Notice this does not depend on the $\sigma_i.$)

Our immediate goal is to exploit this result to compute

$$G(\rho,\sigma_1,\sigma_2) = \iint_{x_1\gt 0,\, x_2\gt 0} x_1x_2 f(x_1,x_2,\rho,\sigma_1,\sigma_2)\,\mathrm dx_1\mathrm dx_2$$

for $-1 \lt \rho \lt 1$ and $\sigma_i\gt 0.$ We will eventually make use of the fact that the $\sigma_i$ are scale parameters, which implies

$$G(\rho,\sigma_1,\sigma_2) = \sigma_1\sigma_2 G(\rho, 1, 1)$$

for all positive $\sigma_i.$

Write

$$\rho^\prime = (1-\rho^2)^{-1/2}.$$

Setting $\sigma_i = \rho^\prime$ makes $F$ particularly simple:

$$F(\rho,\rho^\prime,\rho^\prime) = \frac{1}{2\pi\rho^\prime} \iint_{x_1\gt 0,\, x_2\gt 0}\exp\left[-\frac{1}{2}\left(x_1^2 - 2\rho x_1 x_2 + x_2^2\right)\right]\,\mathrm dx_1\mathrm dx_2.$$

Because the integrand is rapidly decaying and smooth, we may differentiate the integral with respect to $\rho$ by differentiating its integrand:

$$\begin{aligned} \frac{\mathrm d}{\mathrm d \rho}(\rho^\prime F(\rho,\rho^\prime,\rho^\prime)) &= \iint_{x_1\gt 0,\, x_2\gt 0}\frac{\mathrm d}{\mathrm d \rho}\exp\left[-\frac{1}{2}\left(x_1^2 - 2\rho x_1 x_2 + x_2^2\right)\right]\,\mathrm dx_1\mathrm dx_2 \\ &= -G(\rho,\rho^\prime,\rho^\prime). \end{aligned}$$

Computing the derivative (bearing in mind that $\rho^\prime$ is a function of $\rho$) yields

$$\begin{aligned} G(\rho,\sigma_1,\sigma_2) &= \frac{\sigma_1\sigma_2}{(\rho^\prime)^2} G(\rho,\rho^\prime,\rho^\prime)\\ &=\frac{\sigma_1\sigma_2}{2\pi}\left(1 + \frac{2\rho}{\sqrt{1-\rho^2}} \arctan\left(\sqrt{\frac{1+\rho}{1-\rho}}\right)\right). \end{aligned}$$

The value of your second expectation therefore is

$$E[X_1X_2\mid X_1\gt 0,\ X_2\gt 0] = \frac{G(\rho,\sigma_1,\sigma_2)}{F(\rho,\sigma_1,\sigma_2)}.$$

Because $(-X_1,X_2)$ has a bivariate normal distribution (with the same $\sigma_i$) and correlation $-\rho,$ change $\rho$ to $-\rho$ everywhere in this formula to obtain your first expectation.

As a quick check, for independent standard normal variables where $\sigma_1=\sigma_2=1$ and $\rho=0,$ we easily compute $G(0,1,1)=1/(2\pi)$ and $F(0,1,1)=1/4,$ giving $2/\pi$ for the conditional expectation when both variables are positive. Its square root equals the unconditional expectation of $|X_i|,$ as it should.

self-studytag or the question will likely be closed. $\endgroup$