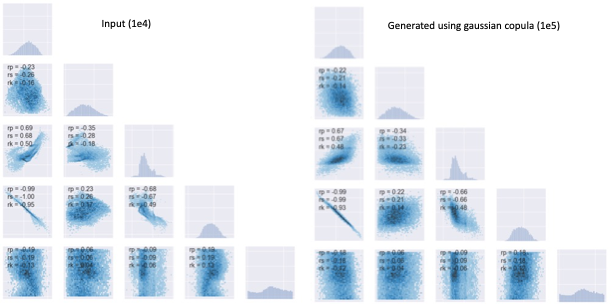

i have a very small set of data, which is a collection of vectors with 4 element (for the sake of simplicity). the 4 marginal distributions are quite diversify (they are gaussian-like or sine-like). from these data, i:

- (scale the data to their arimethic mean and sd) computed their covariance matrix.

- generated a 4-dimensional gaussian using the said cov matrix.

- using cdf of standard gaussian (loc=0, scale=1), i transform the marginal of the said gaussian into uniform distribution (plotting these marginals pairwise give you the copula)

- I used the uniform distribution to perform inverse sampling from my input marginal distribution.

i expected the method work, because copula only capture the correlation, and not marginal. while the generated one tends to be agree well with the input one in terms of marginal distribution and correlation, but pair plot distribution seems very different. (see figure)

am i doing things improperly ? can someone point out ?

i can share the code if you want more information.