An instrumental variable Z is a legitimate instrument for T (the treatment) if the following hold:

- Z has a causal effect on Y that is fully mediated by T (i.e. no direct effect from Z to Y, and the flow of causation must at least run through T)

- Z has no backdoor paths to Y.

- Monotonicity (higher values in the instrument lead to higher values of the treatment being uptaken)

- A 1st stage actually exists (there is a nonzero correlation between Z and T).

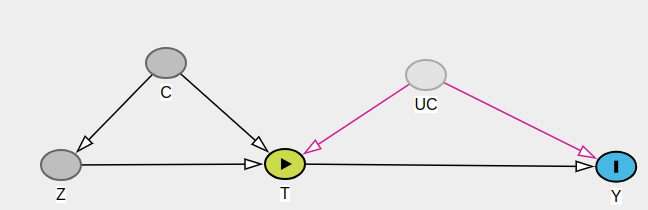

What happens, however, if we have the following DAG?

C is a confounding variable between the treatment and instrument. UC is a set of unobserved confounders. Is Z still a legitimate instrument for T? I was under the impression that the answer is no, but according to https://dagitty.net/dags.html#

...both C and Z are legitimate instruments for T. I can see C being a legitimate instrument since all causal pathways run through T (either directly or mediated by Z). How can Z still be an instrument for T without conditioning on C first, however? I can jump to T through C. Most sources seem to suggest that T and Z must be d-separated, but just wanted to verify this.