I want to calculate the Mean absolute percentage error (MAPE) for my copula model. I am stuck at the forecasting step. I am not specifying the copula here for different data pairs.

- I have two time series

XandY. I found the bestGARCHparameters $\alpha$ and $\beta$ assuming0mean. - The Kendals tau between two variables is $\tau$

- Then I found the best copula and had its parameters say $\kappa$ and $\omega$.

- Now for forecasting, I need to generate residuals using my copula parameters found in step 3.

How to do this if I want to enter the copula parameters MANUALLY and not use some param=fit type of code in R.

I can work in R as well as Excel. Please if somebody could help me with the exact steps of point 4.

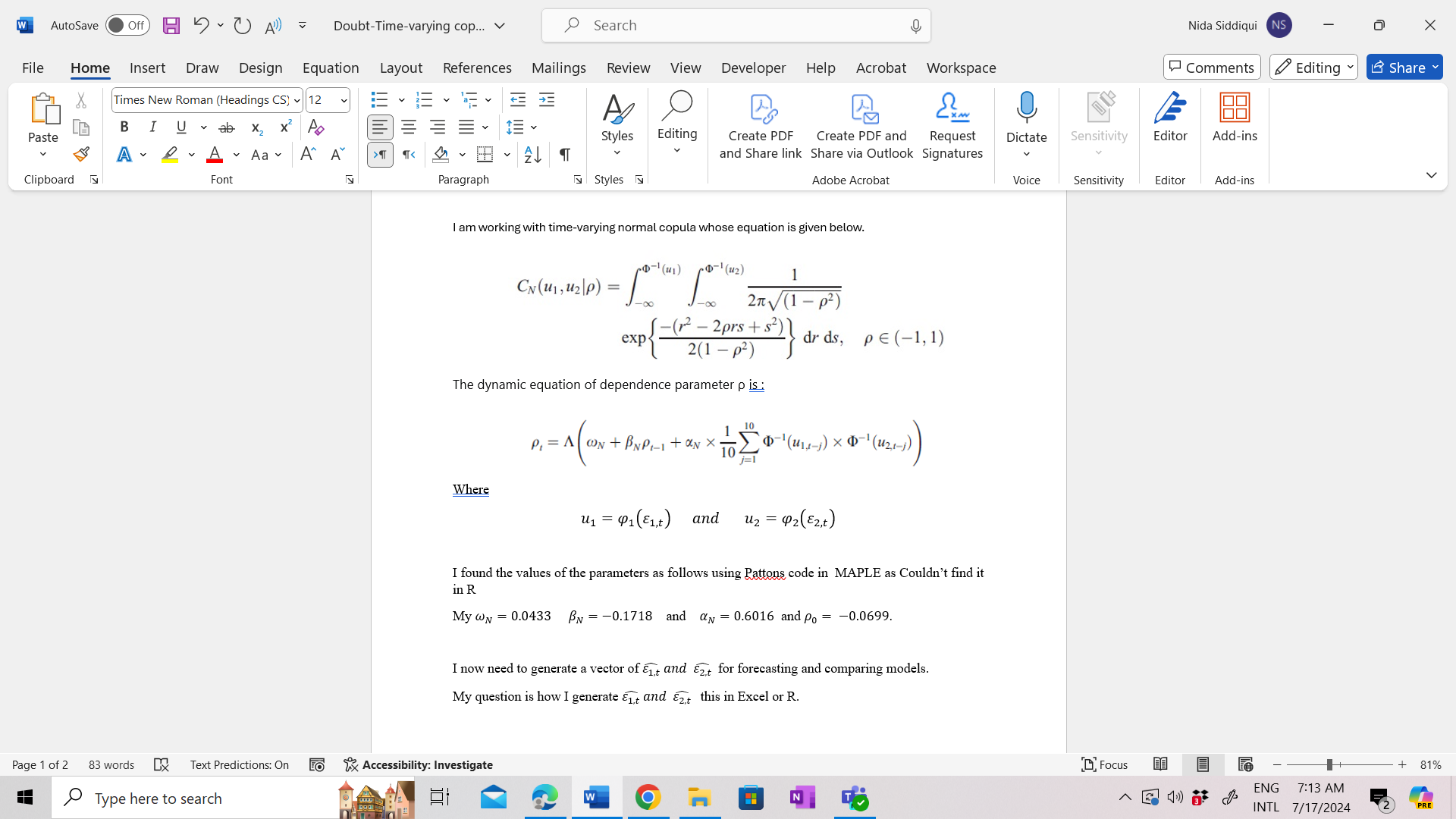

Problem Attachment-  More details attachment-

More details attachment-

Original paper- Patton (2006)- See page 542

sim_fitted-copula <- rCopula(n=your_sample_size, your_fitted_copula(the estimated parameters of the fitted copula))for example, if your fitted copula was Clayton with parameters equal 5. Then,Sim <- rCopula(1000, claytonCopula(5,dim=3)) ## 3 is the dimension of your data, and n=the sample size. $\endgroup$Λ? Please provide more details. $\endgroup$