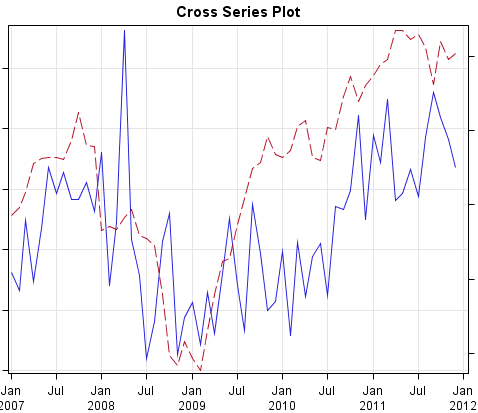

I have 2 (monthly) time-series that look like this:

Economical intuition suggests that they are positively related and I can see this on the plot but if I compute correlation between their log-returns $\ln x_t/x_{t-1}$ and $\ln y_t/y_{t-1}$ this correlation is -0.04 this is basically zero and not statistically significant for my data size (~60 points).

How can it be?

One may say that series are cointegrated $y_t = a x_t +\varepsilon_t$, but then returns should follow $\Delta y_t = a \Delta x_t +\Delta \varepsilon_t$ and correlation between returns would also be significant. So if I see zero correlation between returns, there is no cointegration between levels as well - right?

So does this zero correlation means that there is no relation between series? If yes - why do they follow each other so closely.. If no - how to quantify this relation if correlation between diff'ed series is ~0 and cointegration tests for original series are inconclusive.

EDITS:

-- added cointegration -> correlation link to address @AlecosPapadopoulos question.