I need to sample from the following mixture of two distributions:

$h_{\vec{\beta}}(r)=c(\vec{\beta})[(1-w_{m,\tau}(r))f_{\vec{\beta_{0}}}(r)+w_{m,\tau}(r)g_{\epsilon,\sigma}(r)]$

where $c(\vec{\beta})$ is a normalizing constant, $f_{\vec{\beta_{0}}}$ is the Gamma distribution, $g_{\epsilon,\sigma}$ is the Generalized Pareto distribution, and $w_{m,\tau}$ is the CDF of the Cauchy distribution: $1/2 +(1/\pi)*arctan[(r-m)/\tau]$, acting here as a weight/mixing function providing a smooth transition between the Gamma and Pareto (hence the adjective "dynamic" to qualify the mixture).

The weights allow having one unified mixture where the Gamma captures the bulk of the data, and as we get closer to the extremes, the Pareto takes over control. The approach originated in Figressi et al. (2002), and I have adopted the implementation presented in Vrac and Naveau (2007).

I have estimated the parameters $\vec{\beta}=(m,\tau,\gamma,\lambda,\epsilon,\xi)$, respectively the location and scale of the Cauchy CDF, shape and rate of the Gamma, and shape and scale of the GPD, following the procedure based on MLE described in the second paper referenced (R code can be found here), and now I want to sample from $h_{\vec{\beta}}$. Since the proportions of each component of the mixture are not fixed, I cannot just randomly sample from one distribution or the other (e.g., using using the rgamma() or rgpd() R functions) like is done here or here. So, how should I proceed?

If I could determine the CDF of the mixture, I could use inversion sampling ($U(0,1)$). EDIT: as noted by Xi'an in the second thread listed right below there is no closed form solution for the CDF.

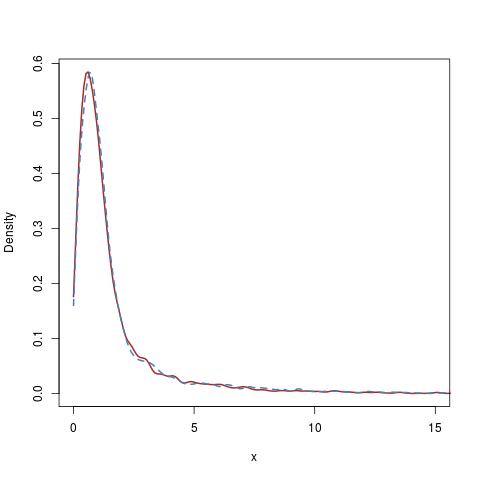

EDIT: implementation of one of the two strategies in Xi'an's answer (rejection sampling) for my data here and Monte Carlo approach to estimating the quantile function of the mixture here.