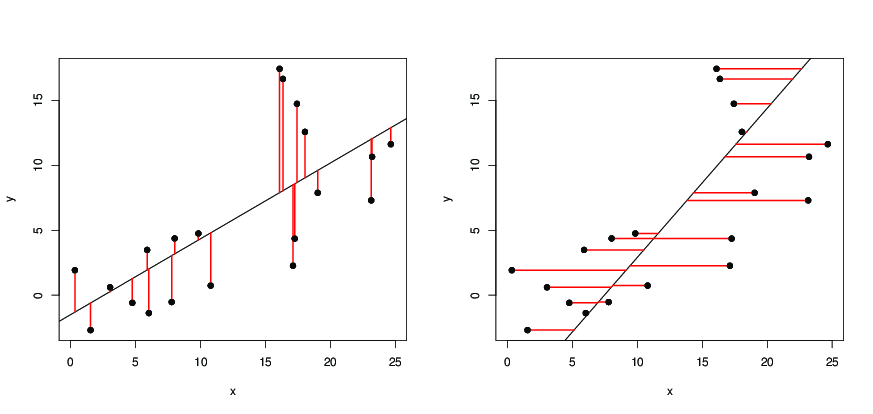

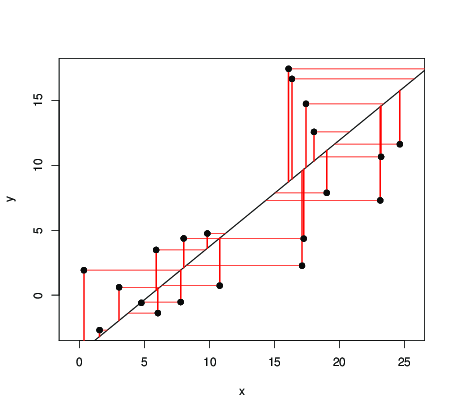

Regression line is not (always) the same as true relationship

You may have some 'true' causal relationship with an equation in a linear form $a+bx$ like

$$y := a + bx + \epsilon$$

Where the $:=$ means that the value of $a+bx$ with some added noise $\epsilon$ is assigned to $y$.

The fitted regression lines y ~ x or x ~ y do not mean the same as that causal relationship (even when in practice the expression for one of the regression line may coincide with the expression for the causal 'true' relationship)

More precise relationship between slopes

For two switched simple linear regressions:

$$Y = a_1 + b_1 X\\X = a_2 + b_2 Y$$

you can relate the slopes as following:

$$b_1 = \rho^2 \frac{1}{b_2} \leq \frac{1}{b_2}$$

So the slopes are not each other inverse.

Intuition

The reason is that

- Regression lines and correlations do not necessarily correspond one-to-one to a causal relationship.

- Regression lines relate more directly to a conditional probability or best prediction.

You can imagine that the conditional probability relates to the strength of the relationship. Regression lines reflect this and the slopes of the lines may be both shallow when the strength of the relationship is small or both steep when the strength of the relationship is strong. The slopes are not simply each others inverse.

Example

If two variables $X$ and $Y$ relate to each other by some (causal) linear relationship $$Y = \text{a little bit of $X + $ a lot of error}$$

Then you can imagine that it would not be good to entirely reverse that relationship in case you wish to express $X$ based on a given value of $Y$.

Instead of

$$X = \text{a lot of $Y + $ a little of error}$$

it would be better to also use

$$X = \text{a little bit of $Y + $ a lot of error}$$

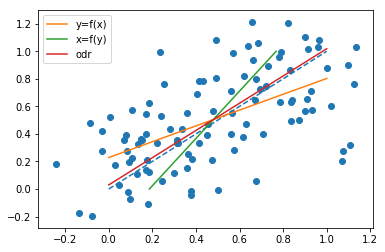

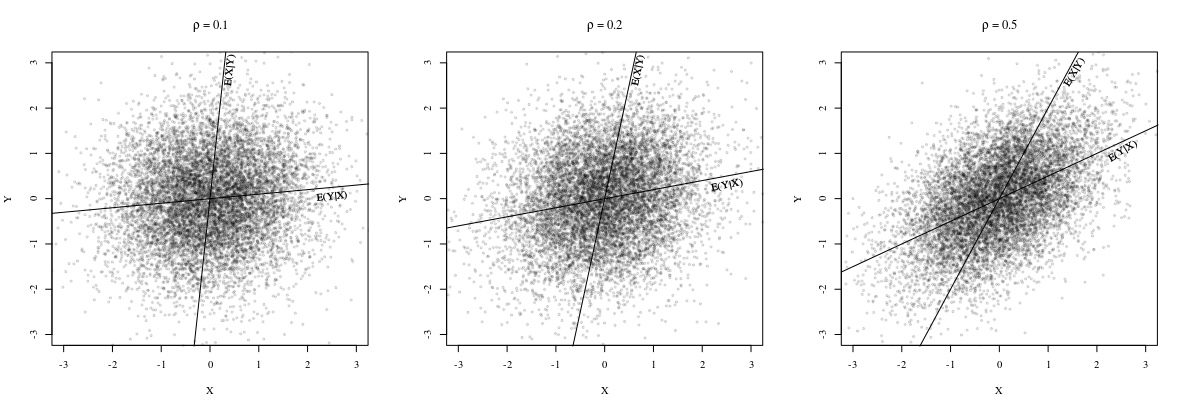

See the following example distributions with their respective regression lines. The distributions are multivariate normal with $\Sigma_{11} \Sigma_{22}=1$ and $\Sigma_{12} = \Sigma_{21} = \rho$

The conditional expected values (what you would get in a linear regression) are

$$\begin{array}{} E(Y|X) &=& \rho X \\

E(X|Y) &=& \rho Y

\end{array}$$

and in this case with $X,Y$ a multivariate normal distribution, then the conditional distributions are

$$\begin{array}{} Y|X & \sim & N(\rho X,1-\rho^2) \\

X|Y & \sim & N(\rho Y,1-\rho^2)

\end{array}$$

So you can see the variable Y as being a part $\rho X$ and a part noise with variance $1-\rho^2$. The same is true the other way around.

The larger the correlation coefficient $\rho$, the closer the two lines will be. But the lower the correlation, the less strong the relationship, the less steep the lines will be (this is true for both lines Y ~ X and X ~ Y)