I am aware that box-cox transformation may make data set significantly normal distributed with constant mean and variance. But sometimes fails to convert data into normal. My question is even though box-cox transformation can not make data significantly normal, it is always make variance and mean constant?

$\begingroup$

$\endgroup$

6

-

$\begingroup$ None of the methods work in all situations and under all circumstances, and I would not expect Box-Cox transformation to be an exception to the rule. $\endgroup$– Richard HardyCommented Jun 11, 2019 at 12:43

-

$\begingroup$ You are right but only method on Google is box cox. Whenever I search for variance stabilization box cox always pop up. That is why I consult you. Could tell me what are the other possible methods to make variance stabilize? $\endgroup$– mertcanCommented Jun 11, 2019 at 16:43

-

$\begingroup$ It does not necessarily make variance constant (see: Alternatives to one-way ANOVA for heteroskedastic data). $\endgroup$– gung - Reinstate MonicaCommented Jun 14, 2019 at 19:49

-

$\begingroup$ Not necessarily, but many boxcox algos actually use a 3-parameter normal distribution so that, even for data that are heteroscedastic across a range of predictors, you can estimate a simple exponential rule (including log) that gives you a change of variable that is somewhat heteroscedastic. $\endgroup$– AdamOCommented Jun 14, 2019 at 19:59

-

$\begingroup$ which is precisely why I said "may" in my answer /comments. . $\endgroup$– IrishStatCommented Jun 14, 2019 at 20:00

|

Show 1 more comment

1 Answer

$\begingroup$

$\endgroup$

4

1) You say "I am aware that box-cox transformation MAY make data set significantly normal distributed with constant mean and variance."

No it simply decouples a possible relationship between the variance of the errors and the Expected value. Please read my answer to When (and why) should you take the log of a distribution (of numbers)?. It MAY generate a more normal distribution if the series is leptokurtric (fat tails)

2) You say/ask "does it is always make variance and mean constant?"

Not necessarily as the error variance may change deterministically over time requiring Generalized Least Squares (Weighted least Squares see http://docplayer.net/12080848-Outliers-level-shifts-and-variance-changes-in-time-series.html ) or stochastically over time requiring a GARCH add-on.

The reason Box-Cox shows up is that in the "old bad days ! " that is all that was known or in textbooks as a way to treat heteroscedastic errors. Textbooks are out of date as soon as they get printed. SE is the true textbook because it is ever evolving to improve the craft .

Also see a number of my posts where the error variance changes and in particular Removing Variance in Time Series After Applying Log Transformation might be of interest and Box Cox Transformation makes Out of sample Forecast Error worse? .

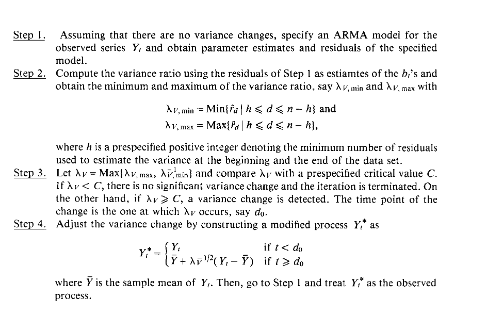

Finally an examination of why intervention detection may be more useful that a box-cox transformation. http://www.autobox.com/pdfs/vegas_ibf_09a.pdf (slide 14 + )

EDITED after remarks

-

$\begingroup$ Those must have been awfully old textbooks, because weighted least squares has been around for a couple of centuries :-). $\endgroup$– whuber ♦Commented Jun 14, 2019 at 19:40

-

$\begingroup$ but it took TSAY to suggest it as treatment for arima errors and even then didn't label it as Weighted Least Squares $\endgroup$ Commented Jun 14, 2019 at 19:48

-

$\begingroup$ Where does the question have anything at all to do with ARIMA errors? Quite clearly it's far more general than that. $\endgroup$– whuber ♦Commented Jun 14, 2019 at 19:49

-

$\begingroup$ agreed ... all I was politely saying was that his treatment of non-constant variance for a set of residuals was to bootstrap the weights based upon evidented variance changes . This significant contribution is what motivated me as a developer/publisher to broadcast it's important value $\endgroup$ Commented Jun 14, 2019 at 19:53