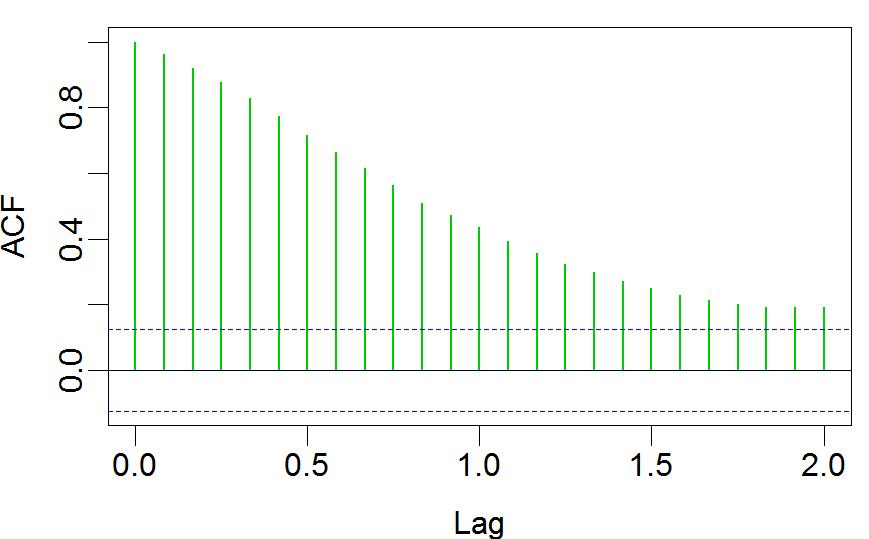

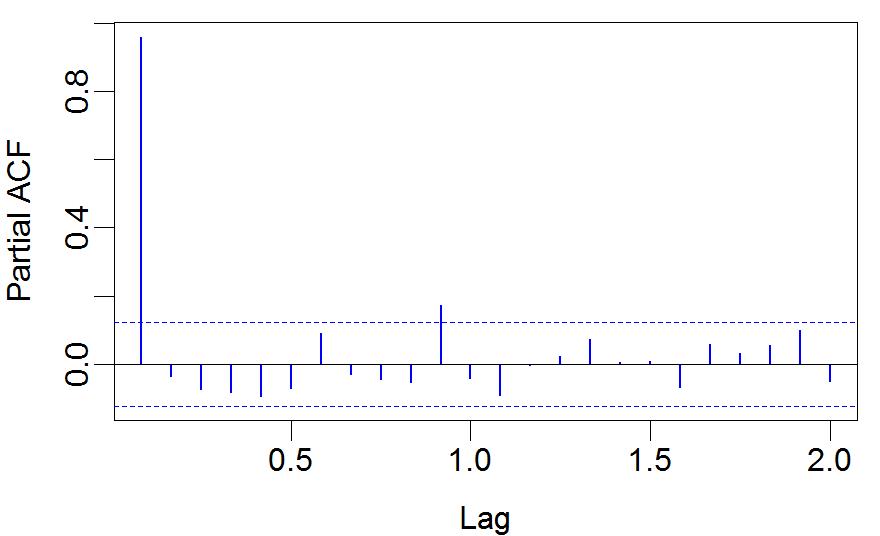

I was thinking, from the ACF it looks like a nonstationary process. Or is it an AR process? From the PACF, does that mean it is AR(1)? There are 2 significant spikes in the PACF. I'm confused.

I was thinking, from the ACF it looks like a nonstationary process. Or is it an AR process? From the PACF, does that mean it is AR(1)? There are 2 significant spikes in the PACF. I'm confused.

Firstly, you should have integer values on the x-axis...

The ACF suggests there is long memory present in the data set. You might try to estimate it - have a look at the options.

In terms of PACF, it suggests what is the order of autocorrelation in the series, but in this case the spike is at 10th and personally, I would assume that AR(1) with $x_{t-10}$ won't really explain much. But it depends what sort of data is it on, maybe it makes sense...

1 on the axis stands for 1 year. Also, why long memory? Looks like ACF has an exponential (rather than linear) decay, hence short memory.

$\endgroup$

Commented

Oct 18, 2016 at 8:52

~ unit root and similar shape :) You want to take natural logarithm and then difference those to get logarithmic differences - thats' what finance works with. Try that and have a look at the ACF and PACF again.

$\endgroup$