I'm trying to filter a time series, of which I occasionally can observe the state variable variable but not always. I also have a noisy measure of this state variable all the time. By picking the time points when I have both, I can compute the error between the two, which gives me a sense of what the noisy measure is like.

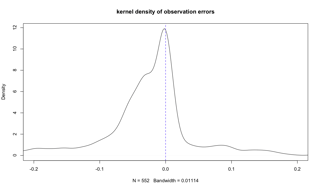

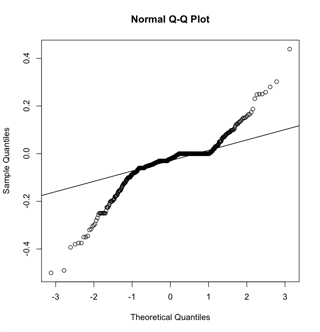

The distribution of error seems to be both skewed and fat-tailed. Based on my rudimentary understanding of Kalman filter, this type of error process would violate the the assumption of normally distributed errors, and using just mean and variance would be biased because the first two moments of the probability distribution are not suffice to characterize the whole thing. I have two questions.

(1) if I don't have other good approaches for now and insist on using Kalman filter, what risk am I taking? Or in other words, how does this kind of distribution affect the accuracy of Kalman filter.

(2) Since the parameters of the measurement equation has to be estimated as well (both coefficients and error variance), I was thinking about using Box-Cox transformation to fix the skew and fit it to a t-distribution. Can I then estimate the parameters online using MLE of t-distribution.