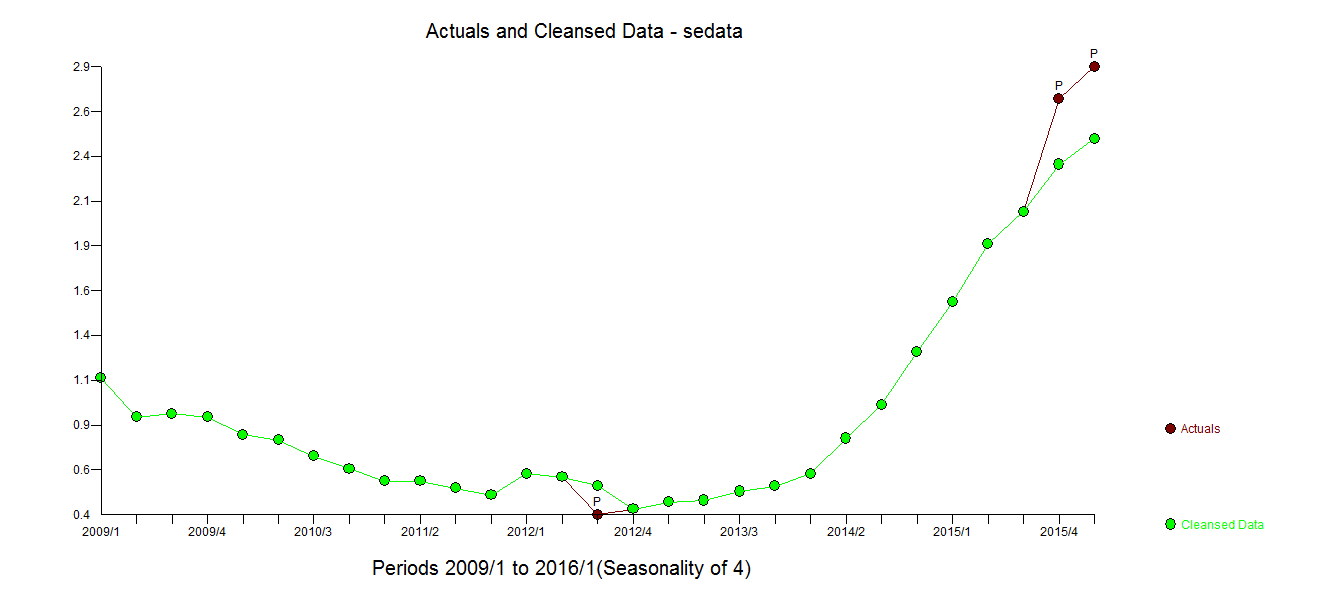

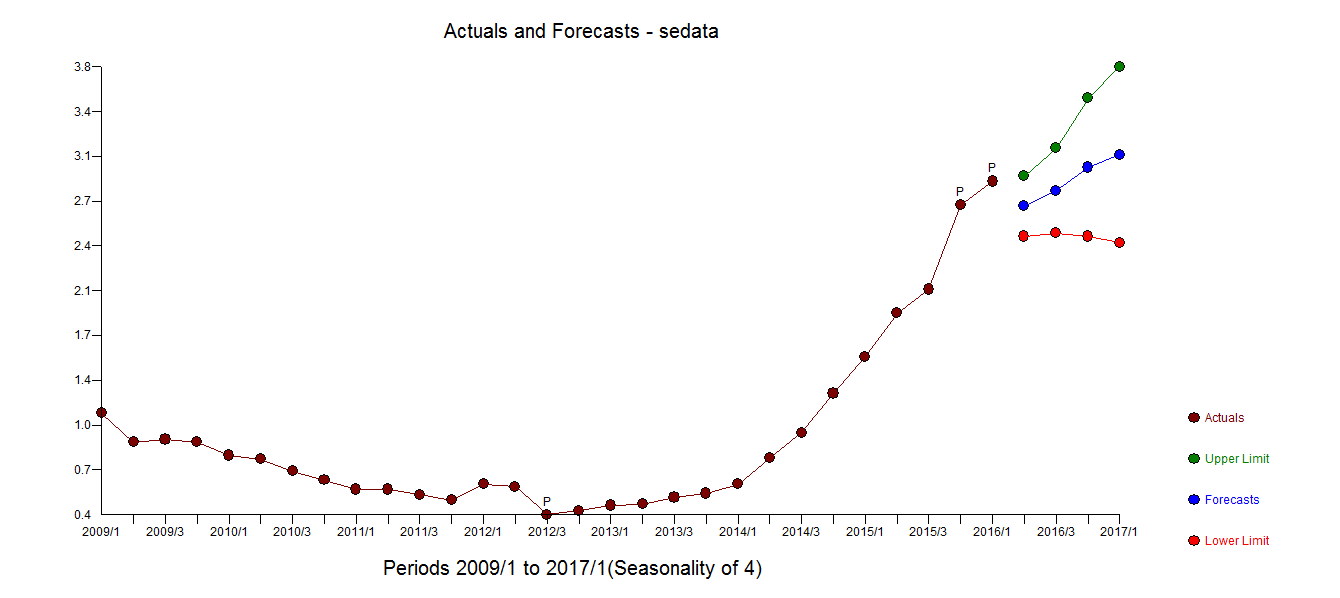

I have some trouble with a specific time series. The time series itself is pretty short: Only 73 observations that look like this:

First problem: Detrend or not?

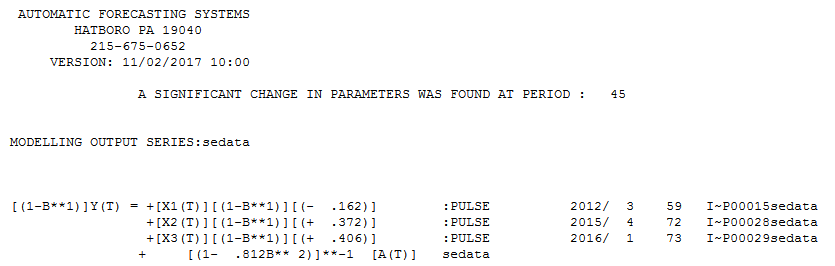

First I need to find out if the time series has a unit root or not. Using the augmented Dickey-Fuller Test the null hypothesis cannot be rejected, therefore I have to assume that the time series has a unit root. Based on this paper one should check this result with another test because the time series is pretty short.

Using the Philips-Perron Test I get the same result (again: the time series has a unit root) but using the KPSS Test I get a contradicting result. Based on the KPSS Test one cannot reject the null hypothesis which states that the time series has no deterministic trend.

I know that unit root and deterministic trend are two different things that are hard to distinguish. But overall I would say that the time series has a trend.

Second problem: Take logarithm or not?

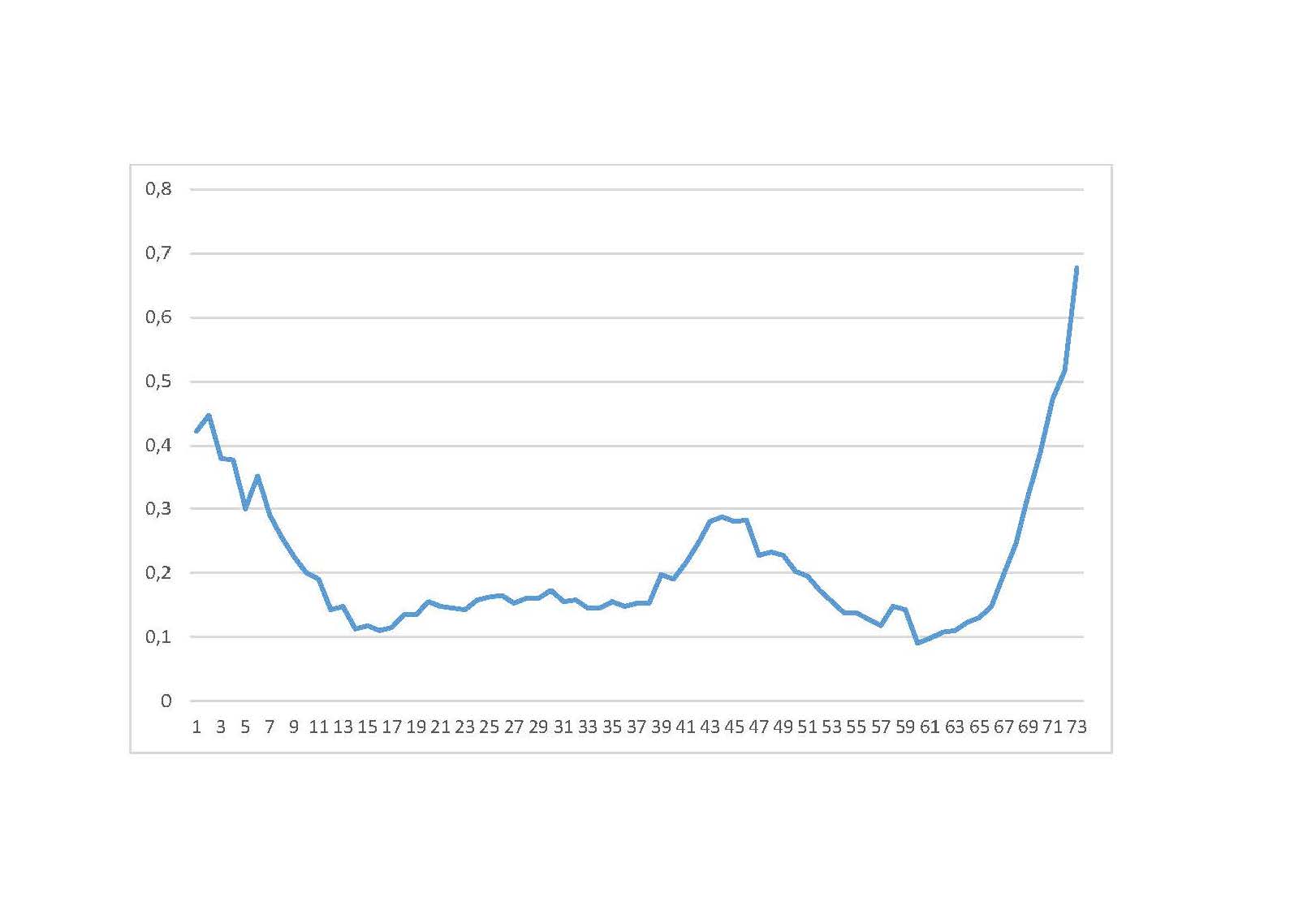

For many time series (e.g., GDP) one has to take the logarithm first because most detrending methods (e.g., Hodrick-Prescott Filter) are linear filters. Apart from that GDP looks pretty exponential so taking log first is probably not the worst idea. But for some time series, especially interest rates or a share of two variables (which is the case for my time series), one does not take the logarithm. But why? Detrending my time series with and without taking the natural logarithm first I get totally different results for the trend and the cyclical component.

Why would I bother?

The reason I have to detrend the time series is that I want to analyze the time series over a business cycle. Therefore if I want to compare (or merge) different business cycles I have to detrend the series from non-cyclical aspects.

To be honest using log first gives better results – but I don't think this is a valid basis on which to answer these questions.