In the following passage of A Map and Simple Heuristic to Detect Fragility, Antifragility, and Model Error by Nassim Taleb:

Convexity Effects and Jensen's Inequality

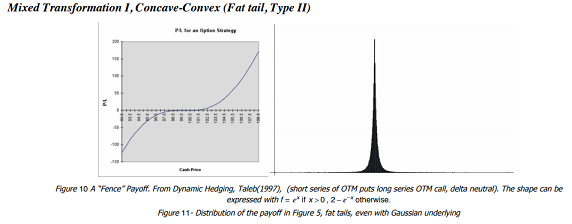

Define a convex function as one with a positive second derivative, but this is a mathematical construct that does not translate well into practice (as it requires twice-differentiability). Recall from Figure 10

the “flipping” of the exposure from convex in the body of the distribution to severely concave in the tails. So, more practically, convexity over an interval $2 \Delta x$ satisfies the following inequality:

$$\frac{1}{2}\left( f(x+\Delta x) +f(x-\Delta x \right)\geq f(x)$$

Why economics as a discipline made the monstrously consequential mistake of treating estimated parameters as nonstochastic variables and why this leads to fat-tails even while using Gaussian models.

The average of expectations is not the expectation of an average. For $f$ convex across all values of $\{X_i\},$

$$\sum w_i E \Big [f(X_i)\Big ] \geq E\Big [\sum f(w_i X_i)\Big ]$$ For example, take a conventional die (six sides) and consider a payoff equal to the number it lands on. The expected (average) payoff is $\frac{1}{6} \sum_{i=1}^6 i = 3.5 .$ Now consider that we get the squared payoff, $\frac{1}{6} \sum_{i=1}^6 i^2 = \frac{91}{6} \approx15.67,$ while I $\frac{1}{6} \left( \sum_{i=1}^6 i \right)^2= 12.25,$ so, since squaring is a convex function, the average of a square payoff is higher than the square of the average payoff.

The question is:

With the example of the die and the difference between the square of the expectation and the expectation of the squares, he is just calculating the variance. Is this a valid example of Jensen's inequality?