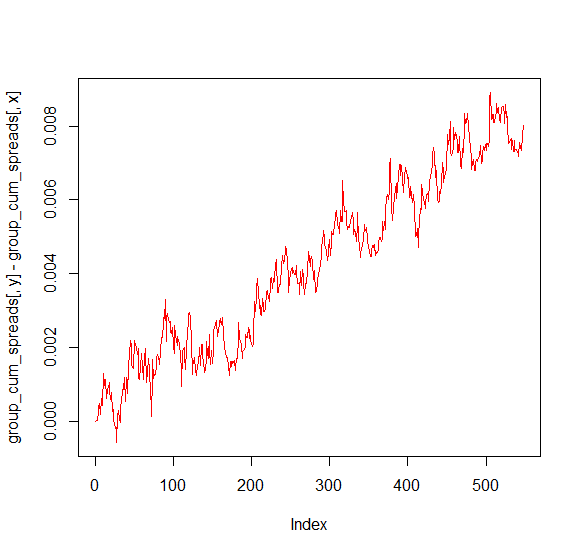

On a first glance your data seems to be trend stationary. That means that if you subtract the trend (in this case a straight line with positive slope) from the time-series you will have a stationary time series. Trend stationary data is not stationary before you subtract the trend.

Also note the official RDocumentation:

The general regression equation which incorporates a constant and a linear trend >is used and the t-statistic for a first order autoregressive coefficient equals >one is computed. The number of lags used in the regression is k. The default >value of trunc((length(x)-1)^(1/3)) corresponds to the suggested upper bound on >the rate at which the number of lags, k, should be made to grow with the sample >size for the general ARMA(p,q) setup. Note that for k equals zero the standard >Dickey-Fuller test is computed. The p-values are interpolated from Table 4.2, p. >103 of Banerjee et al. (1993). If the computed statistic is outside the table of >critical values, then a warning message is generated.

Missing values are not allowed

There are some exceptions, e.g. missing values.

Furthermore here:

What is the difference between a stationary test and a unit root test?

and here:

Contradictory results of ADF and KPSS unit root tests

and here:

ADF test, PP test, KPSS test: Which test to prefer?

I already explained situations, in which the Nullhypothesis of an ADF-test is rejected and a time series is not-stationary. You should apply a KPSS test for stationarity as well.

Reject unit root, reject stationarity: both hypothesis are component hypothesis >– heteroskedasticity in series may make a big difference; if there is structural >break it will affect inference.