If we have an autocorrelated variable in the multiple regression model, why does taking first difference help?

1

-

2$\begingroup$ First differencing will remove the effects of a linear trend from estimates of autocorrelation. That is the only circumstance where first differencing is guaranteed to remove autocorrelation. $\endgroup$– whuber ♦Commented Jun 18, 2019 at 20:33

Add a comment

|

1 Answer

$\begingroup$

$\endgroup$

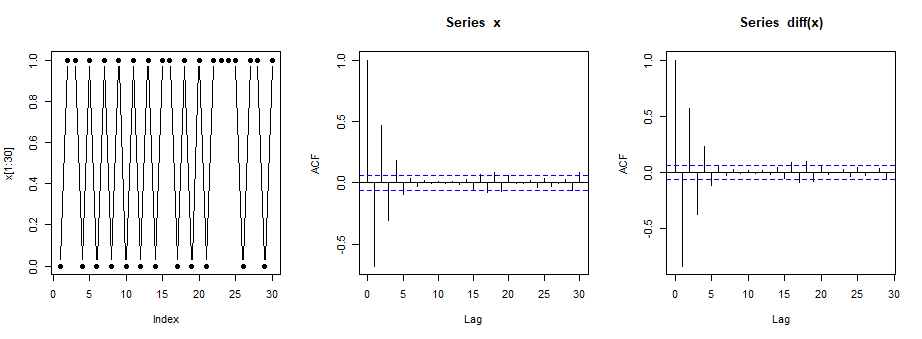

I don't know the nature of the autocorrelation in your application. However, taking differences does not, in general, mitigate autocorrelation.

Here is an example with a simple Markov chain:

set.seed(618)

m = 1000; x = numeric(m); x[1] = 0

for (i in 2:m)

{

if (x[i-1] == 0) x[i] = rbinom(1,1,.9)

else x[i] = rbinom(1,1,.2)

}

table(x)

x

0 1

458 542

x[1:16]

[1] 0 1 1 0 1 0 1 0 1 0 1 0 1 0 1 1

diff(x)[1:15]

[1] 1 0 -1 1 -1 1 -1 1 -1 1 -1 1 -1 1 0

par(mfrow=c(1,3))

plot(x[1:30], type="b", pch=19) # first 30 steps

acf(x)

acf(diff(x))

par(mfrow=c(1,1))