The elastic net paper (here) introduced the naive-elastic net and elastic net. The coefficient estimates of naive-elastic net are obtained by solving the problem $$\hat\beta_{naive-enet}=\text{argmin}_\beta \big\lVert y - X\beta\big\rVert^2 + \lambda_1\lVert \beta\rVert_1 + \lambda_2 \lVert \beta\rVert^2_2.$$ The elastic net is a scaled version of the naive-elastic net: $\hat\beta_{enet} = (1+\lambda_2)\hat\beta_{naive-enet}$.

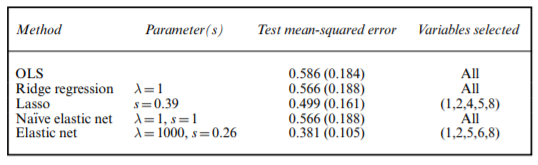

But I'm confused about the prostate data analysis in Section 4 of the paper. According to the definition above, the naive-elastic net and elastic net must select the same variables since the scaling above does not change non-zero coefficients. Hence, in the data analysis, the elastic net should have selected all the variables since the naive-elastic net included all the variables in the model. But the authors reported different selected-variables for these estimators in Table 1. How is this possible? (The picture below is from the paper.)

I know that different parameters give different models. But the elastic net is two-step process: 1. fit a naive-elastic net and 2. rescale the fitted naive-elastic net. If I get a naive-elastic net model with all the variables at the 1st step, I should get the model with the same variables in the 2nd step!