Given:

$X \sim \mathcal{N}(\mu, \sigma^2)$

$Y|X=x \sim \mathcal{N}(0, (\theta x)^2)$

$Z = X + Y$

I want to be able to make hypothesis tests or confidence intervals for $\mu$ using $Z$ and known $\theta$ and $\sigma^2$. For example, I draw $z = 950$, and I have $\sigma^2 = 10000$ and $\theta = 0.10$. How would I estimate a confidence interval for $\mu$ with this information?

Edit:

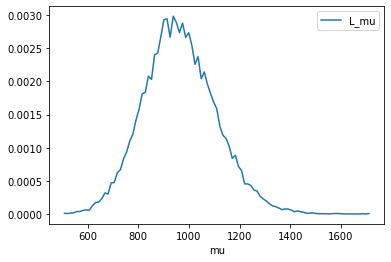

I'm not really sure how to go about this analytically, but I've been able to create confidence intervals numerically. Here's an empirical plot of the likelihood of $\mu$ given the observed $z$ and parameters in the above example.

Code for the above plot:

import scipy.stats as stats

import numpy as np

import pandas as pd

x_var = 10000

theta = 0.10

samples = int(4e7)

df1 = pd.DataFrame(index=range(samples))

df1['mu'] = stats.uniform.rvs(size=samples)*1500+500

df1['x'] = stats.norm.rvs(loc=df1['mu'] , scale=np.sqrt(x_var) , size=samples)

df1['y'] = stats.norm.rvs(loc=0 , scale=np.abs(theta*df1['x']) , size=samples)

df1['z'] = df1['x'] + df1['y']

z_observed = 950

df1.drop(df1[np.round(df1['z']) != z_observed].index, inplace = True)

hist1 = (pd.DataFrame(np.histogram(df1['mu'],bins=99,density=True))

.transpose().rename(columns={0: 'L_mu', 1: 'mu'}))

hist1.plot(x='mu',y='L_mu')