There are many approaches to modeling integrated or nearly-integrated time series data. Many of the models make more specific assumptions than more general models forms, and so might be considered as special cases. de Boef and Keele (2008) do a nice job of spelling out various models and pointing out where they relate to one another. The single equation generalized error correction model (GECM; Banerjee, 1993) is a nice one because it is (a) agnostic with respect to the stationarity/non-stationarity of the independent variables, (b) can accommodate multiple dependent variables, random effects, multiple lags, etc, and (c) has more stable estimation properties than two-stage error correction models (de Boef, 2001).

Of course the specifics of any given modeling choice will be particular to the researchers' needs, so your mileage may vary.

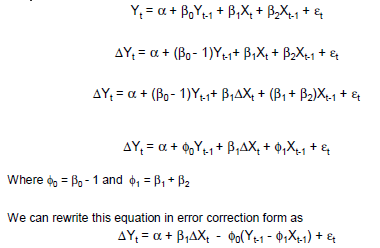

Simple example of GECM:

$$\Delta{y_{ti}} = \beta_{0} + \beta_{\text{c}}\left(y_{t-1}-x_{t-1}\right) + \beta_{\Delta{x}}\Delta{x_{t}} + \beta_{x}x_{t-1} + \varepsilon$$

Where:

$\Delta$ is the change operator;

instantaneous short run effects of $x$ on $\Delta{y}$ are given by $\beta_{\Delta{x}}$;

lagged short run effects of $x$ on $\Delta{y}$ are given by $\beta_{x} - \beta_{\text{c}} - \beta_{\Delta{x}}$; and

long run equilibrium effects of $x$ on $\Delta{y}$ are given by $\left(\beta_{\text{c}} - \beta_{x}\right)/\beta_{\text{c}}$.

References

Banerjee, A., Dolado, J. J., Galbraith, J. W., and Hendry, D. F. (1993). Co-integration, error correction, and the econometric analysis of non-stationary data. Oxford University Press, USA.

De Boef, S. (2001). Modeling equilibrium relationships: Error correction models with strongly autoregressive data. Political Analysis, 9(1):78–94.

De Boef, S. and Keele, L. (2008). Taking time seriously. American Journal of Political Science, 52(1):184–200.