As stated in the GRS paper, you have to estimate the intercepts of each asset in your portfolio by sample OLS. This will give you a vector of estimates $\hat{\alpha}_1, \hat{\alpha}_2, \ldots$. Put these into a vector $\hat{\alpha}$. Now estimate the covariance matrix of the assets in the 'usual' way, calling it $\hat{\Sigma}$. Then compute $W_u = \hat{\alpha}^{\top} \hat{\Sigma}^{-1} \hat{\alpha} / (1 + \hat{\theta}^2),$ where $\hat{\theta}$ is the sample-estimated Sharpe ratio of the market portfolio (the one that you used in the individual OLS regressions as the market). Then $T W_u$ should follow a Hotelling Law, where $T$ is the number of days observed (for the regressions. Note that a modification of the GRS test allows one to use a covariance esimator built on different data from the OLS regressions).

The test statistic is then computed as below:

#compute the sample Sharpe ratio

sample.sr <- function(x) {

mu <- mean(x)

sg <- sd(x)

return(mu / sg)

}

#srets is a T x N matrix of the returns of the assets

# by return, I mean the relative return (V_t / V_{t-1}) - 1,

# where V_t is the 'value' of the asset at time t.

# relative returns make more sense when combined 'laterally'

#mret is a T-vector of the returns of the 'market'

GRS.test <- function(srets,mret) {

T <- dim(srets)[1]

N <- dim(srets)[2]

#this is 'good' R style, but probably slow as hell.

#would be faster to precompute the solution to the

#normal equations and apply it en masse to the srets

#matrix ...

reg.func <- function (y, m) {

mod <- lm(y ~ m)

mod$coefficients["(Intercept)"]

}

alphas <- as.vector(apply(srets, 2, reg.func, mret))

#now the sigma hat;

Sig.hat <- cov(srets)

mkt.sr <- sample.sr(mret)

#the GRS test statistic

W.u <- t(alphas) %*% solve(Sig.hat,(alphas)) / (1 + mkt.sr^2)

#convert to F

F.stat <- T * (T - N - 1) * W.u / (N * (T - 2))

p.val <- pf(F.stat, N, T-N-1, 0, lower.tail = FALSE)

return(list('Wu' = W.u,'Fstat' = F.stat,'pval' = p.val))

}

#generate population data under the null to test the code;

#return the p-value for the data

GRS.gen.null <- function(T,N) {

srets <- matrix(rnorm(T*N),ncol=N)

mret <- as.vector(rnorm(T))

test.it <- GRS.test(srets,mret)

return(test.it$pval)

}

#always test your code under the null!

set.seed(1066)

nday <- 150 #'T'

nstock <- 8 #'N'

ntrial <- 2048 #number of experiments

should.be.p <- replicate(ntrial,GRS.gen.null(nday,nstock))

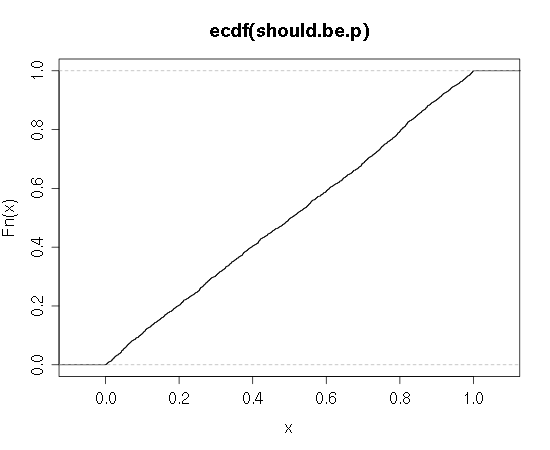

plot(ecdf(should.be.p))

I tested the function under the null hypothesis to confirm uniformity of the resultant p-values. Here is a plot:

This is a brain dead form of the null, where the stocks have no beta as well as no alpha (I was in a hurry). Probably one would want to test the power as well. Also note that using the some matrix math instead of calling lm will probably speed up this code quite a bit.

You can also use the F distribution to compute confidence intervals on the non-centrality parameter (assumed to be zero under the null).

If there is not a stock R package for performing this test, I would be very surprised (and would like to write such a package in that case ... )